Can You Sell Covered Calls In An Ira

Hey, so you're thinking about selling covered calls in your IRA? That's... interesting. A little spicy, even. Let's chat about it like we're grabbing a coffee, okay? No judgment here, just trying to figure out if this is a brilliant idea or one that might make your accountant faint. (Spoiler alert: it can be a bit of both!)

First Things First: What ARE Covered Calls Anyway?

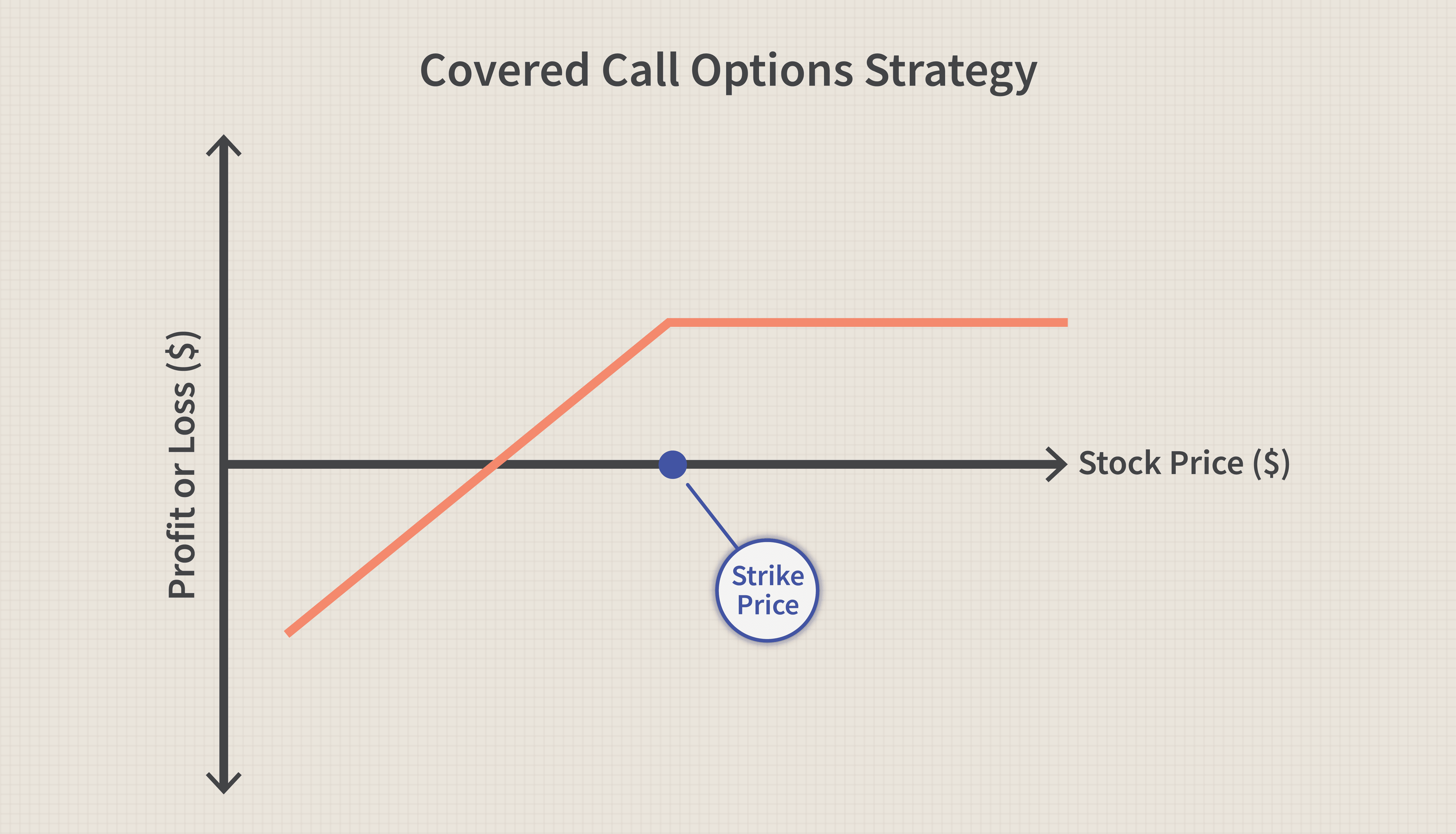

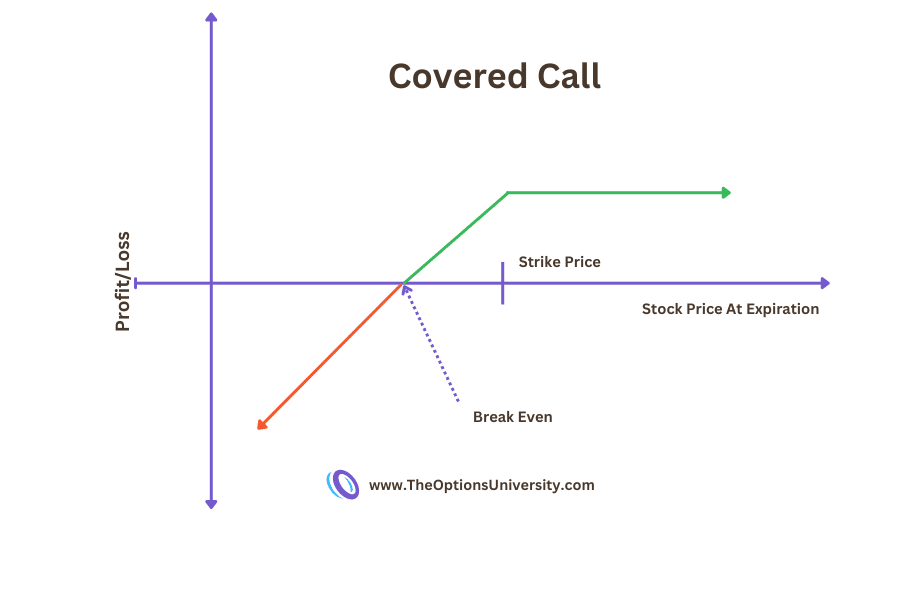

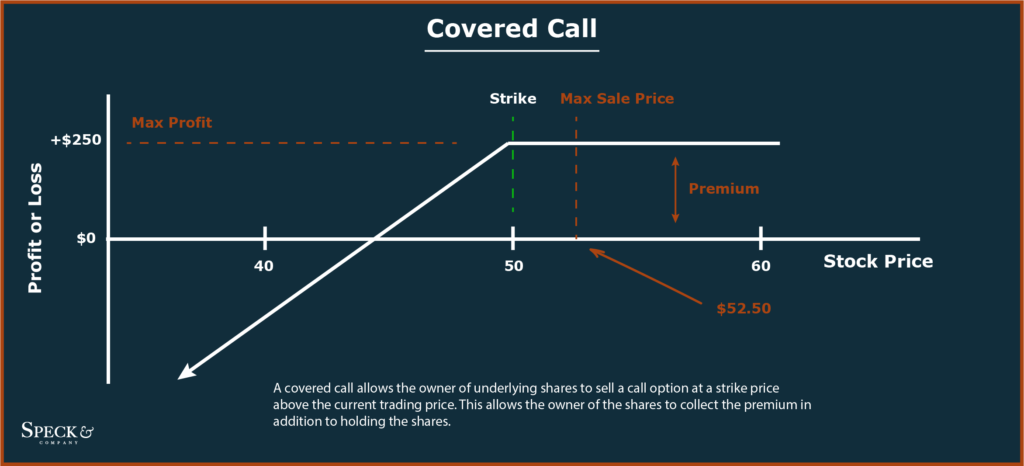

Okay, real quick recap. If you already know this, feel free to skip ahead to the juicy bits. But for those new to the party: A covered call is basically you owning 100 shares of a stock and then selling someone else the option to buy those shares from you at a specific price (the "strike price") by a specific date (the "expiration date").

Think of it like renting out your stock. You get paid a little something (the "premium") upfront for giving someone the chance to buy your shares. If the stock price stays below the strike price, you keep the premium and nothing happens. Yay, free money! If the stock price goes above the strike price, you might have to sell your shares. Less yay, but you still made a profit, right? It's a calculated gamble, a dance with the market, a...well, you get the picture.

Must Read

Can You ACTUALLY Do This in an IRA?

Alright, the million-dollar question (or, you know, the hopefully-more-than-a-million-dollar-IRA question). The short answer is: yes, generally you can. But (and there's always a "but," isn't there?) there are some serious caveats to consider. Think of them as little gremlins lurking in the fine print, waiting to cause trouble.

See, the IRS (those lovely folks we all adore paying taxes to) has rules about what's allowed in an IRA. And they really don't like anything that could be considered "engaging in a trade or business." Which, under certain circumstances, selling options could potentially be viewed as. Dun dun DUN!

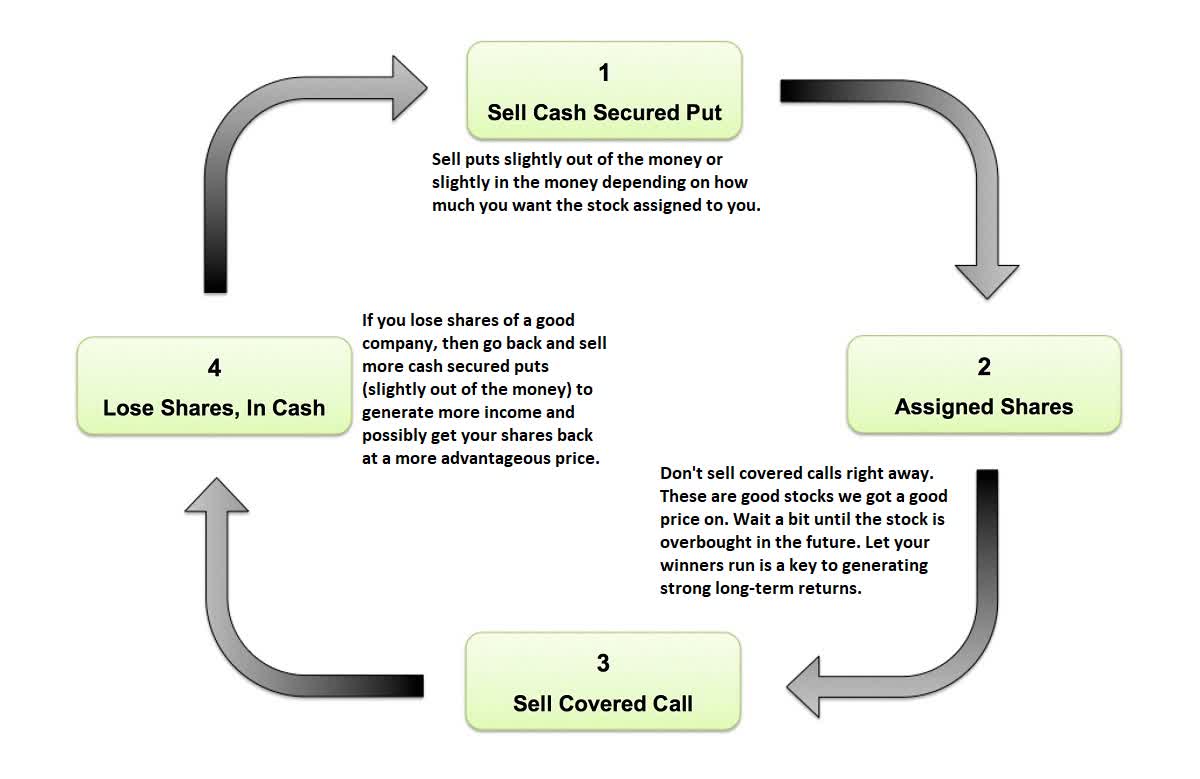

Now, selling covered calls usually flies under the radar because it's considered a pretty conservative strategy. You already own the underlying stock, so you're not taking on a ton of extra risk (at least, not compared to naked calls...we're not even GOING there right now). But it's still important to tread carefully. The last thing you want is the IRS deciding your IRA is actually a business, and suddenly you owe a massive tax bill. Yikes!

The Importance of Your Brokerage Account

Okay, so here's where things get a little more granular. Not all brokerages allow options trading in IRAs. Period. End of story. Some just don't want the hassle, some are more risk-averse, and some probably just haven't updated their systems since the Stone Age. (Okay, slight exaggeration, but you get the point.)

So, the first thing you absolutely MUST do is check with your brokerage. Call them, email them, send a carrier pigeon – whatever it takes. Ask them explicitly if they allow covered call writing in IRAs. If they say no, well, that's that. Time to find a new brokerage! (Or, you know, stick to less exciting investments. But where's the fun in that? Just kidding...mostly.)

And even if they do allow it, make sure you understand their specific rules and requirements. Do they have any restrictions on the types of stocks you can use? Are there limits on the number of contracts you can sell? Are there any special forms you need to fill out? Knowing this upfront can save you a lot of headaches later.

Potential Risks and Considerations (aka, the "Don't Be An Idiot" Section)

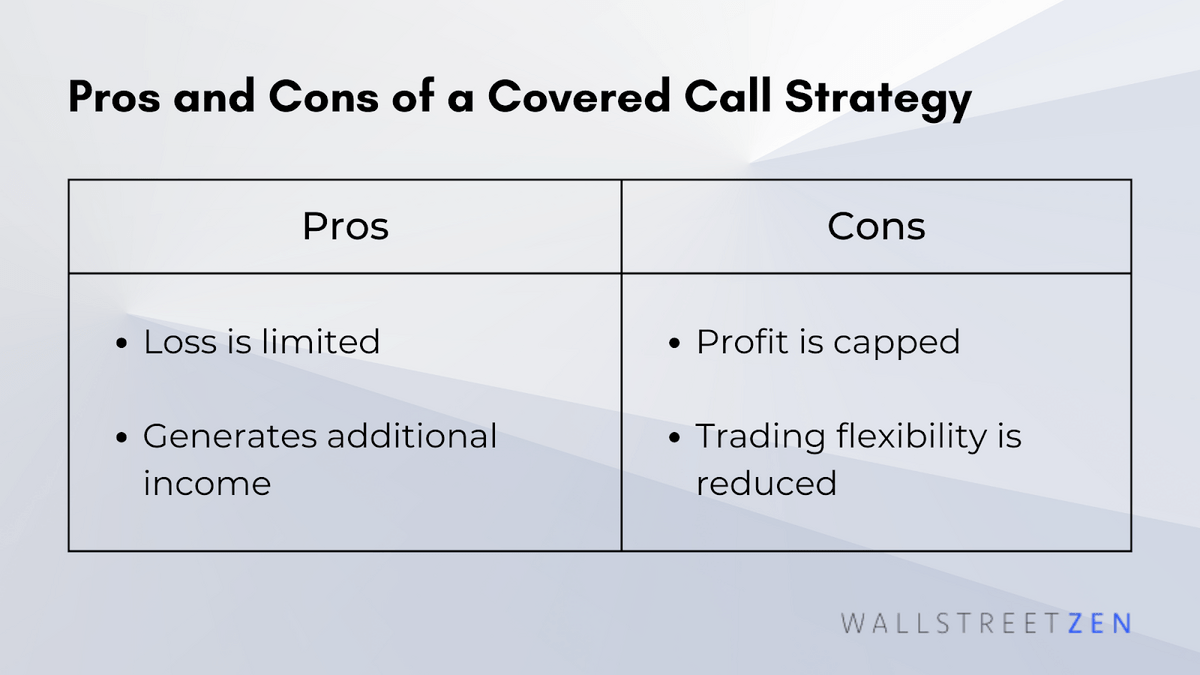

Alright, let's get real for a minute. Selling covered calls can be a great way to generate extra income in your IRA. But it's not a free lunch. There are risks involved, and it's crucial to understand them before you dive in headfirst.

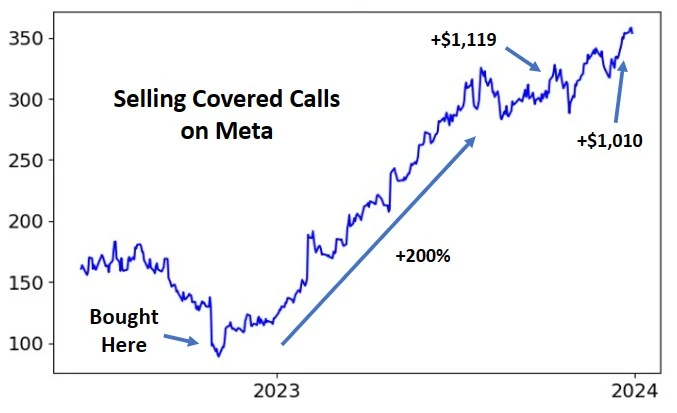

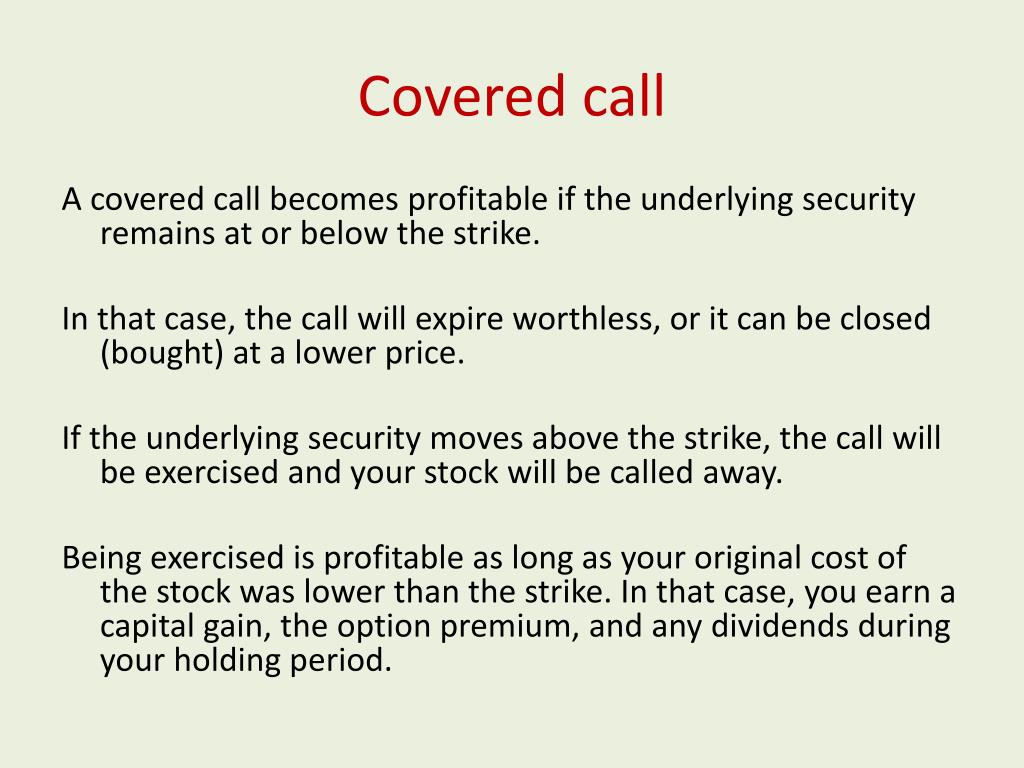

1. The Opportunity Cost: This is probably the biggest one. If the stock price skyrockets above the strike price, you'll be forced to sell your shares at that price, even if they're worth way more. You're essentially capping your potential upside. Ouch! Imagine if you sold covered calls on Apple back in the day...you'd be kicking yourself all the way to the poorhouse (relatively speaking, of course, since you still have an IRA!).

2. Assignment Risk: Even if the stock price is only slightly above the strike price at expiration, you could be assigned. This means you'll have to deliver your shares. It's not the end of the world, but it can be a bit of a hassle. And if you're not paying attention, you might accidentally let your shares get called away without realizing it.

3. Tax Implications (Even in an IRA!): While the profits from selling covered calls within an IRA are generally tax-deferred (or tax-free in a Roth IRA), there can be some tax implications if you're not careful. For example, if your covered call strategy becomes so active that the IRS considers it a business, you could be subject to self-employment taxes. Again, this is unlikely with a simple covered call strategy, but it's something to be aware of.

4. Brokerage Margin Requirements: Some brokerages may require you to maintain a certain amount of margin in your IRA account to cover the potential risks of options trading. This means you'll need to have more cash in your account than just the value of the underlying stock. Make sure you understand your brokerage's margin requirements before you start trading.

Strategies for Staying Safe (and Keeping the IRS Happy)

Okay, so how do you minimize the risks and keep the IRS off your back? Here are a few tips:

* Start Small: Don't go all-in right away. Begin with a small number of contracts and gradually increase your position size as you gain experience and confidence. Think of it as dipping your toes in the water, not cannonballing into the deep end.

* Choose High-Quality Stocks: Stick to well-established, blue-chip stocks with a history of stable performance. Avoid highly volatile stocks or penny stocks, as these can be much riskier to trade options on.

* Select Realistic Strike Prices: Don't be greedy! Choose strike prices that are slightly above the current stock price. This will give you a better chance of keeping your shares and collecting the premium. Selling calls with strike prices far above the current price may bring in more premium, but it also greatly increases the chance of missing out on potential gains.

* Manage Your Positions Actively: Don't just set it and forget it. Monitor your positions regularly and be prepared to adjust them as needed. If the stock price starts to move against you, you may need to roll your contracts to a later expiration date or a higher strike price.

* Keep Good Records: This is always a good idea, but it's especially important when trading options in an IRA. Keep track of all your trades, including the dates, strike prices, premiums, and any commissions you pay. This will help you stay organized and make it easier to file your taxes (if necessary).

* Consult With a Financial Advisor: If you're not sure whether selling covered calls in your IRA is right for you, talk to a qualified financial advisor. They can help you assess your risk tolerance, understand the potential risks and rewards, and develop a strategy that's tailored to your specific needs.

The Bottom Line: Is It Worth It?

So, after all that, is selling covered calls in an IRA a good idea? It depends. (I know, I know, that's the most annoying answer ever. But it's true!)

If you're a conservative investor looking for a way to generate extra income in your IRA without taking on excessive risk, then it might be worth considering. But it's crucial to do your research, understand the risks, and follow the strategies outlined above.

On the other hand, if you're a risk-averse investor or you're not comfortable with options trading, then it's probably best to stick to more traditional investments. There's no shame in playing it safe! Remember, the goal is to grow your IRA over the long term, not to get rich quick (or, more likely, poor quick!).

Ultimately, the decision is yours. Just make sure you make an informed decision, not an impulsive one based on some get-rich-quick scheme you saw on the internet. (Yes, I'm talking to you!).

Now, go forth and conquer the market! (But please, do it responsibly.) And if you have any more questions, feel free to ask. I'm always happy to chat about investing over a virtual cup of coffee.

Disclaimer: I'm not a financial advisor, so this is not financial advice. Consult with a qualified professional before making any investment decisions. Investing involves risk, and you could lose money. Blah blah blah...you know the drill.