Can K 1 Losses Offset Ordinary Income

Understanding how losses from Schedule K-1 can offset your ordinary income is crucial for effectively managing your tax liability, particularly if you're an investor or business owner involved in partnerships, S corporations, or limited liability companies (LLCs) taxed as partnerships or S corporations. Here's a practical guide to navigating this complex area.

Understanding K-1 Losses

Schedule K-1 is a tax form used to report a partner's or shareholder's share of income, losses, deductions, and credits from a pass-through entity. A K-1 loss means that the entity you're invested in experienced a loss, and a portion of that loss is allocated to you. The crucial question is whether you can use this loss to reduce your taxable income, and if so, to what extent.

Passive vs. Non-Passive Activities

The key factor determining whether you can deduct a K-1 loss against your ordinary income is whether the activity generating the loss is considered passive or non-passive. The IRS defines a passive activity as a trade or business in which you do not materially participate. Material participation generally means you are involved in the operation of the business on a regular, continuous, and substantial basis.

Must Read

Think of it this way: If you're actively involved in running the business, it's likely non-passive. If you're primarily an investor who doesn't actively manage the day-to-day operations, it's likely passive.

If the activity is non-passive, you can generally deduct the full amount of the K-1 loss against your ordinary income, subject to certain other limitations (which we'll discuss below). This is particularly relevant for those actively involved in their businesses.

However, if the activity is passive, the deductibility of the loss is subject to the passive activity loss (PAL) rules. These rules are designed to prevent taxpayers from using losses from passive investments to shelter income from active businesses or wages.

Passive Activity Loss (PAL) Rules

Under the PAL rules, you can only deduct passive losses to the extent you have passive income. In other words, passive losses can offset passive income. If your total passive losses exceed your total passive income, the excess losses are suspended and carried forward to future years.

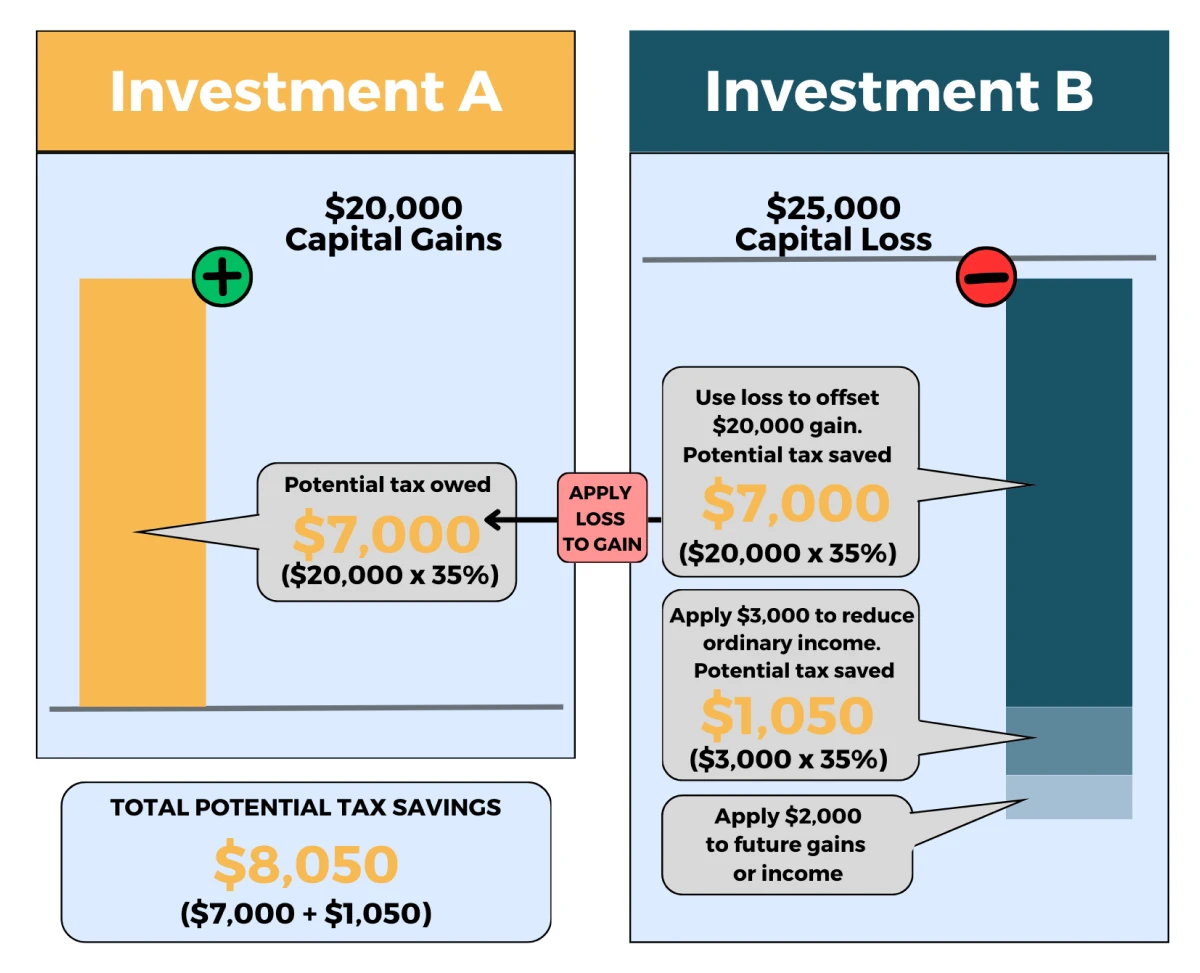

Example: Passive Loss Scenario

Let's say you receive a K-1 showing a $5,000 loss from a passive investment in a real estate limited partnership. You also have $2,000 of passive income from another investment. In this case, you can only deduct $2,000 of the $5,000 loss. The remaining $3,000 is a suspended passive loss that you can carry forward to future years.

What Happens to Suspended Losses?

Suspended passive losses are not lost forever. They can be carried forward indefinitely and used to offset passive income in future years. Furthermore, when you eventually sell your entire interest in the passive activity, any remaining suspended losses become fully deductible in that year, regardless of whether you have passive income. This is a significant benefit for long-term investors.

Special Rule for Real Estate Professionals

There's a significant exception to the passive activity rules for real estate professionals. If you qualify as a real estate professional, rental real estate activities you participate in are not automatically treated as passive. To qualify, you must meet two tests:

- More than half of the personal services you perform in all trades or businesses during the year are performed in real property trades or businesses in which you materially participate.

- You perform more than 750 hours of services during the year in real property trades or businesses in which you materially participate.

If you meet these tests, your rental real estate activities are treated as non-passive, and you can deduct losses from these activities against your ordinary income, subject to other limitations like the excess business loss rules (explained below).

The $25,000 Rental Real Estate Exception

Even if you don't qualify as a real estate professional, you may be able to deduct up to $25,000 of losses from rental real estate activities if you actively participate in those activities. Active participation is a lower standard than material participation and generally means you make management decisions, such as approving tenants, deciding on rental terms, and approving repairs. This $25,000 exception is phased out if your adjusted gross income (AGI) exceeds $100,000 and is completely eliminated when your AGI reaches $150,000.

Other Limitations on Deductibility

Even if your K-1 loss passes the passive activity loss tests, it may still be subject to other limitations, such as the at-risk rules and the excess business loss rules.

At-Risk Rules

The at-risk rules limit the amount of losses you can deduct to the amount you have at risk in the activity. Your at-risk amount generally includes the cash and the adjusted basis of other property you contribute to the activity, as well as any amounts you've borrowed for the activity for which you are personally liable. This prevents you from deducting losses exceeding your actual economic investment in the activity.

Excess Business Loss Rules

The excess business loss (EBL) rules, introduced by the Tax Cuts and Jobs Act of 2017, further limit the amount of business losses that noncorporate taxpayers (individuals, estates, and trusts) can deduct. For 2023, the EBL limit is $289,000 for single filers and $578,000 for married filing jointly. Any business losses exceeding these limits are disallowed and carried forward as a net operating loss (NOL) to future years.

Example: Excess Business Loss

You are married filing jointly and have a K-1 loss of $650,000 from a business in which you actively participate. Your business income is $100,000. This results in a business loss of $550,000 ($100,000 - $650,000). The EBL limit for married filing jointly is $578,000. You can deduct $550,000, leaving no excess business loss.

However, if your K-1 loss was $800,000 instead, then your business loss will be $700,000 ($100,000 - $800,000). You can only deduct $578,000 due to the excess business loss limitation. The remaining $122,000 ($700,000 - $578,000) is carried forward as an NOL.

Practical Application and Tips

- Track Your Passive Activities: Maintain detailed records of all your passive activities, including income, losses, and any suspended losses carried forward.

- Understand Material Participation: Carefully assess your level of involvement in each business to determine whether it's passive or non-passive. Document your participation.

- Consider Real Estate Professional Status: If you're heavily involved in real estate, evaluate whether you meet the requirements to qualify as a real estate professional.

- Plan for Dispositions: When considering selling an interest in a passive activity, remember that any suspended losses become deductible in the year of sale. Factor this into your financial planning.

- Consult a Tax Professional: Given the complexity of these rules, seeking professional advice from a qualified tax advisor is highly recommended. They can help you navigate these rules and optimize your tax strategy.

Checklist/Guideline for K-1 Loss Deductibility

- Identify K-1 Losses: Review your Schedule K-1 forms to identify any losses reported.

- Determine Passive vs. Non-Passive: Assess whether each activity is passive or non-passive based on your level of involvement.

- Apply PAL Rules: If passive, determine if you have sufficient passive income to offset the losses.

- Carry Forward Suspended Losses: Track any suspended passive losses for future use.

- Consider Real Estate Rules: Evaluate eligibility for the real estate professional exception or the $25,000 rental real estate exception.

- Check At-Risk Rules: Ensure your deductible losses do not exceed your at-risk amount in the activity.

- Apply Excess Business Loss Rules: Determine if your losses are subject to the EBL limitations.

- Consult a Tax Advisor: Seek professional guidance to ensure compliance and optimize tax benefits.