Bad Credit Credit Union Personal Loans

Access to credit is a cornerstone of modern financial life, enabling individuals to purchase homes, finance education, and manage unexpected expenses. However, for individuals with bad credit, securing a loan can feel like an insurmountable challenge. Credit unions, often touted as member-centric alternatives to traditional banks, sometimes offer personal loans to those with less-than-perfect credit histories. This article explores the causes, effects, and broader implications of bad credit personal loans offered by credit unions.

Causes: Why Individuals Seek Bad Credit Loans

The demand for bad credit personal loans arises from a confluence of factors. Primarily, it stems from a lack of access to traditional financing options. A low credit score, typically resulting from late payments, defaults, high credit utilization, or even a limited credit history, automatically disqualifies many applicants from obtaining loans from banks and other mainstream lenders.

The 2008 financial crisis significantly tightened lending standards. Even as the economy recovered, many institutions remained wary of extending credit to individuals perceived as high-risk. This caution left a significant segment of the population underserved, creating a vacuum that alternative lenders, including some credit unions specializing in this niche, have attempted to fill.

Must Read

Unexpected financial hardships also drive individuals towards bad credit loans. Medical bills, job loss, or unexpected home repairs can quickly deplete savings and force individuals to seek immediate financial assistance, even if it means accepting less favorable loan terms. A 2023 study by the Federal Reserve found that nearly 40% of American adults would struggle to cover an unexpected $400 expense, highlighting the vulnerability of many households to financial shocks.

Finally, a lack of financial literacy contributes to the problem. Individuals may not fully understand the impact of their credit behavior, leading to poor financial decisions that damage their credit scores. Furthermore, they may not be aware of alternative options like credit counseling or debt management programs that could help them improve their financial standing.

Effects: The Impact of Bad Credit Credit Union Loans

Bad credit personal loans offered by credit unions can have both positive and negative effects on borrowers. On the positive side, they can provide access to much-needed funds during emergencies. This can be crucial for covering essential expenses or preventing further financial deterioration. For example, a loan might allow someone to repair their car, enabling them to continue working and earning income.

Furthermore, successfully repaying a bad credit loan can help rebuild a damaged credit score. Regular, on-time payments are a significant factor in credit scoring models, and a consistent track record of responsible repayment can demonstrate creditworthiness to future lenders.

However, the negative effects often outweigh the benefits. Bad credit loans typically come with significantly higher interest rates and fees than traditional loans. This increased cost of borrowing can trap borrowers in a cycle of debt, making it difficult to repay the loan and further damaging their credit.

For instance, a borrower with a credit score below 600 might face an interest rate of 25% or higher on a personal loan, compared to rates of 10% or less for borrowers with excellent credit. This difference can translate to thousands of dollars in additional interest payments over the life of the loan.

The structure of some bad credit loans can also be problematic. Some lenders may offer loans with short repayment terms or balloon payments, which can be difficult for borrowers to manage. If a borrower is unable to make a payment, they may incur late fees and penalties, further compounding their financial difficulties.

The availability of bad credit loans can also create a moral hazard. Some individuals may be tempted to take out loans for unnecessary purchases or to finance unsustainable lifestyles, leading to further debt and financial instability.

Credit Union Specific Considerations

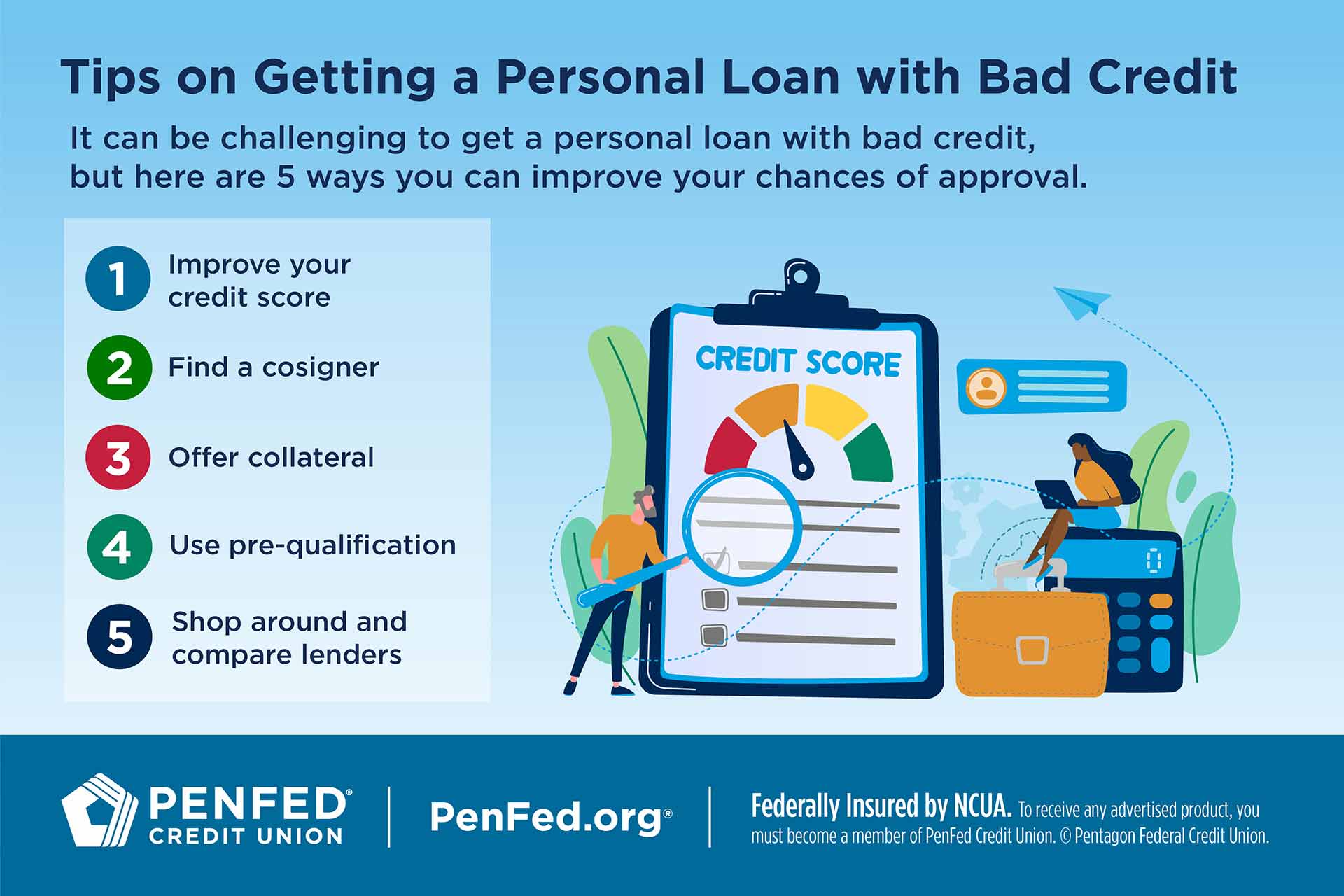

While credit unions often promote themselves as offering fairer terms, the reality can be nuanced. Some credit unions, particularly smaller ones with limited resources, may still offer bad credit loans with high rates to offset the perceived risk. However, many credit unions distinguish themselves by offering financial literacy programs and counseling services to members, helping them manage their finances and improve their credit scores.

Membership requirements are also a factor. To obtain a loan from a credit union, individuals must typically become members, which may involve meeting certain eligibility criteria, such as living or working in a specific geographic area or belonging to a particular organization. This can limit access for some individuals.

Implications: Broader Societal and Economic Consequences

The widespread availability of bad credit loans has significant implications for society and the economy. It can exacerbate income inequality by disproportionately burdening low-income individuals with high-cost debt. This can hinder their ability to build wealth and improve their financial well-being.

Furthermore, the prevalence of debt can contribute to financial instability and economic vulnerability. When a large segment of the population is struggling to manage debt, it can reduce consumer spending and slow economic growth. It also increases the risk of defaults and foreclosures, which can have ripple effects throughout the economy.

The proliferation of predatory lending practices, including those associated with some bad credit loan providers, raises ethical concerns. While not all credit unions engage in such practices, it's important to be aware of the potential for exploitation. Regulations aimed at protecting consumers from predatory lending are crucial, but effective enforcement is essential to ensure that these regulations are followed.

The role of credit unions in providing financial services to underserved communities is also a key consideration. Credit unions often play a vital role in providing access to credit and financial services in areas where traditional banks are less prevalent. However, it's important to ensure that these services are offered in a responsible and sustainable manner, without trapping borrowers in cycles of debt.

Financial literacy education is paramount. Equipping individuals with the knowledge and skills to manage their finances effectively is essential to prevent them from falling prey to predatory lending practices and to help them build a more secure financial future. This includes teaching them how to budget, save, manage credit, and understand the terms and conditions of loans.

The long-term solution lies in addressing the underlying causes of bad credit. This includes promoting economic opportunity, increasing access to education and job training, and strengthening the social safety net to help individuals weather financial hardships. By addressing these root causes, we can reduce the demand for bad credit loans and create a more equitable and sustainable financial system.

Broader Significance

The issue of bad credit credit union personal loans touches upon fundamental questions about access to financial resources, economic justice, and the role of financial institutions in society. While these loans can provide a lifeline for some, their potential for harm cannot be ignored. A balanced approach that combines responsible lending practices, robust consumer protections, and comprehensive financial literacy education is essential to ensure that individuals with bad credit have access to fair and sustainable financial solutions. Ultimately, the goal should be to empower individuals to improve their financial well-being and build a more secure future, rather than trapping them in a cycle of debt.