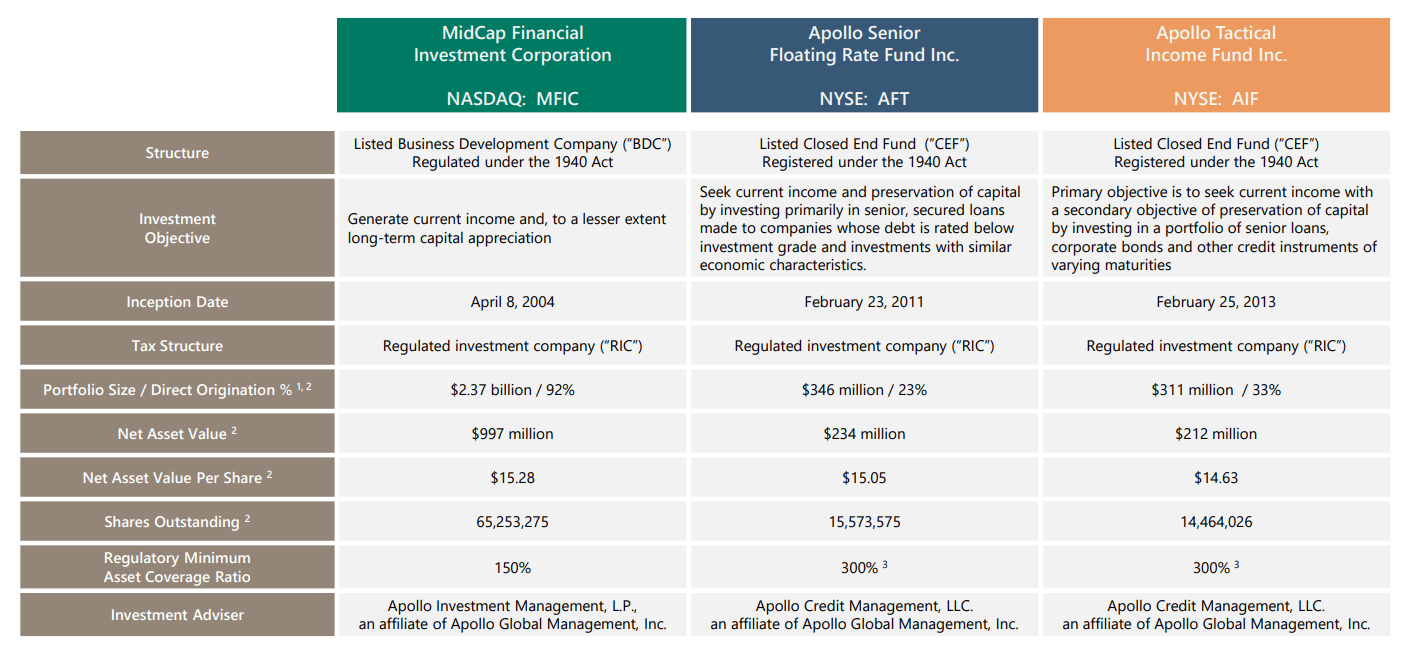

Apollo Senior Floating Rate Fund Inc

Okay, so picture this: I'm at a barbecue last summer, grilling burgers (badly, I admit) and chatting with my neighbor, Dave. Dave, bless his heart, is always looking for the next big thing in investing. This time, he's practically vibrating with excitement about something called a "senior floating rate fund." My eyes glazed over instantly, I'm not gonna lie. But he kept going on about how it was "safe" and "generated income" and "beat inflation"... I figured I should probably at least pretend to be interested. Turns out, he was talking about stuff like the Apollo Senior Floating Rate Fund Inc., which made me think, "huh, maybe I should actually look into this!" (You know, after I managed to salvage the burgers.)

So, let's dive into what exactly this thing is all about. Because honestly, the name itself sounds kinda… intimidating, doesn't it? (I mean, "senior floating rate?" Sounds like something out of a sci-fi movie!). But stick with me, it's not as scary as it sounds.

What IS the Apollo Senior Floating Rate Fund Inc.?

In a nutshell, the Apollo Senior Floating Rate Fund Inc. (ticker: AFT) is a closed-end fund. Now, I know what you're thinking: "Great, another term I don't understand!" Don't worry. A closed-end fund is basically a company that raises a fixed amount of capital through an initial public offering (IPO) and then invests that capital in a portfolio of assets. Unlike mutual funds, which can continuously issue new shares, closed-end funds have a limited number of shares. They trade on the stock exchange just like any other stock.

Must Read

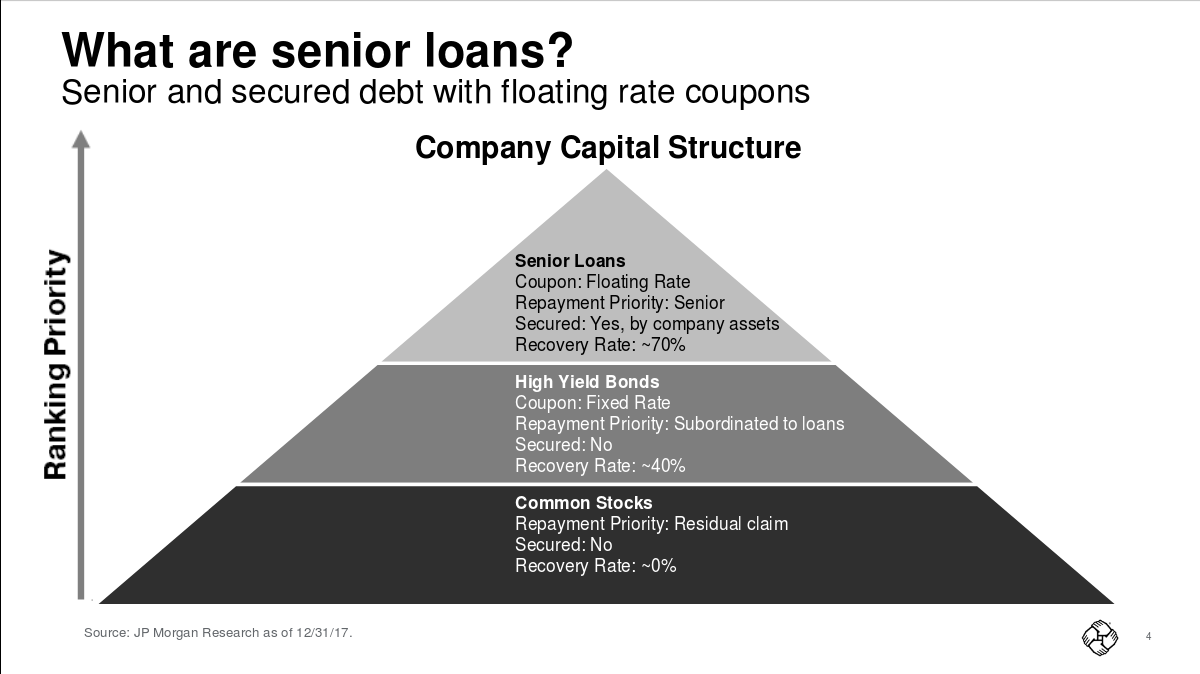

The key thing here is what AFT invests in: primarily senior, secured loans. Think of these as loans that are given to companies that aren't necessarily in the best financial shape. These are often called leveraged loans or bank loans.

Now, you might be thinking, "Wait, that sounds risky!" And you're not wrong! But there's a few mitigating factors:

- Seniority: These loans are "senior," meaning they have priority over other debt if the company goes bankrupt. Think of it as being first in line at the bankruptcy buffet.

- Secured: These loans are "secured," meaning they are backed by collateral. The lender has a right to specific assets of the borrower if the company doesn't repay the loan. Like, they can grab the company's equipment or buildings.

- Floating Rate: This is the kicker. The interest rate on these loans "floats," or adjusts periodically based on a benchmark rate, typically LIBOR (though LIBOR is being phased out, more on that later!). This means that if interest rates rise, the income generated by the fund also rises. That's the magic!

Why Floating Rates Matter (Especially Now)

Remember all the talk about inflation and rising interest rates lately? (It's been pretty hard to miss, right?). Well, that's where these floating rate loans become particularly attractive. When the Federal Reserve raises interest rates to combat inflation, the interest payments on these loans go up accordingly. So, AFT, and similar funds, can potentially provide a hedge against rising interest rates. It's like having a financial shield against inflation! (Okay, maybe not a perfect shield, but definitely a helpful one.)

Digging Deeper: AFT's Portfolio and Strategy

So, we know what AFT invests in, but let's look at how they do it. It's important to remember that Apollo Global Management, a large and established alternative investment manager, manages this fund. So, they’re supposedly the smart guys, right?

Here's a few things to keep in mind about AFT's portfolio and strategy:

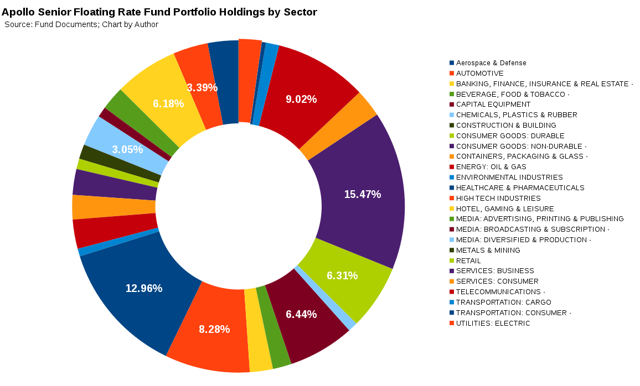

- Diversification: AFT typically invests in a wide range of senior loans across different industries. This diversification helps to reduce risk. (Don't put all your eggs in one precarious basket!).

- Credit Analysis: Apollo's team of credit analysts carefully evaluates the creditworthiness of the companies they lend to. They try to weed out the ones that are likely to default. (Basically, they're trying to pick the least likely to go bankrupt, which is a key job).

- Active Management: The fund is actively managed, meaning that Apollo's portfolio managers are constantly buying and selling loans to try to maximize returns and manage risk. (This is different from a passive index fund that just tracks a market index).

- Leverage: AFT uses leverage, which means they borrow money to invest in more loans. This can amplify both gains and losses. (It's like using a magnifying glass – it can make things bigger, but it can also burn you if you're not careful!). This is definitely a factor to be seriously considered before investment.

Key Considerations and Potential Risks

Okay, let's be real. Nothing is perfect, and that includes the Apollo Senior Floating Rate Fund Inc. There are always risks involved in investing, and it's crucial to understand them before you jump in. Here's a few things to consider:

- Credit Risk: Even with careful analysis, there's always the risk that a company will default on its loan. If that happens, AFT could lose money. (This is the big one, and it's why these loans offer higher interest rates in the first place).

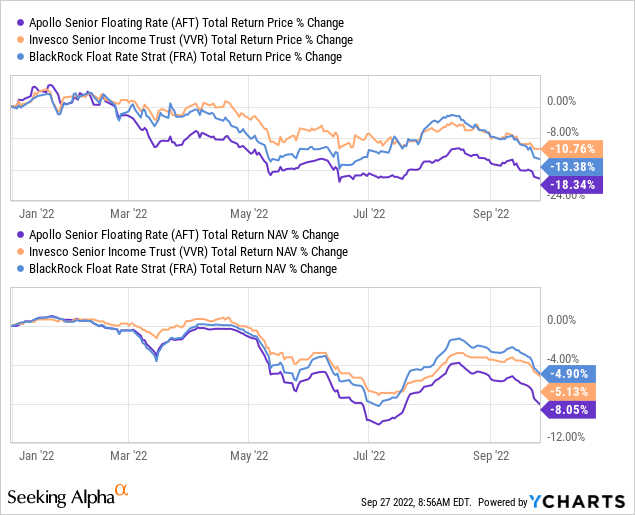

- Interest Rate Risk: While floating rates can protect against rising interest rates, they can also be negatively affected if interest rates fall. (If rates go down, the income generated by the fund will also go down. That's just how it works.).

- Leverage Risk: As mentioned earlier, leverage can amplify both gains and losses. If the fund's investments perform poorly, the leverage will magnify those losses. (Imagine that magnifying glass setting your entire portfolio on fire!).

- Liquidity Risk: Senior loans can be less liquid than other types of investments, such as stocks or bonds. This means that it may be difficult to sell them quickly if AFT needs to raise cash. (Basically, it might be hard to get your money out if you suddenly need it).

- Management Fees: Closed-end funds typically charge higher management fees than passive index funds. These fees can eat into your returns. (You're paying Apollo to manage the fund, and they're not doing it for free!).

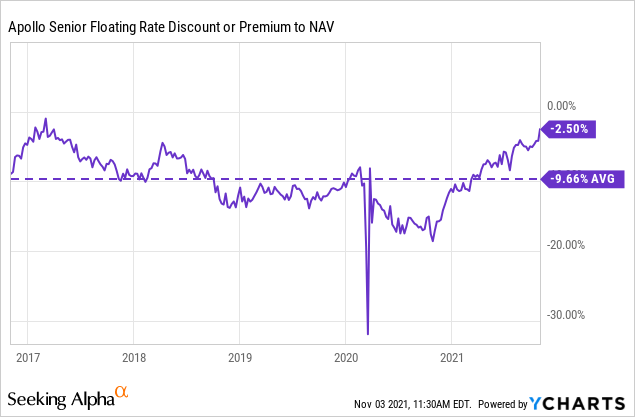

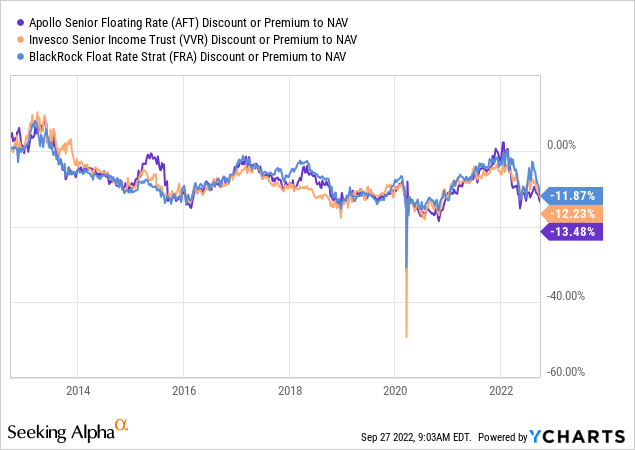

- Discount/Premium to NAV: Closed-end funds trade on the stock exchange, and their price can fluctuate independently of their net asset value (NAV). The NAV is the value of the fund's underlying assets minus liabilities, divided by the number of shares outstanding. AFT can trade at a discount to its NAV (meaning it's trading for less than its assets are worth) or at a premium (meaning it's trading for more). (Buying at a discount sounds great, but it's important to understand why it's trading at a discount!).

- LIBOR Transition: The London Interbank Offered Rate (LIBOR) is being phased out and replaced with alternative reference rates, such as the Secured Overnight Financing Rate (SOFR). This transition could create some uncertainty and potentially affect the value of floating rate loans. (It's like switching from one language to another – there might be some translation issues along the way).

So, is AFT a Good Investment?

That's the million-dollar question, isn't it? (Or, maybe just the slightly-above-average-burger-price question, since we're talking about investing, not winning the lottery!). The answer, as always, is: it depends.

AFT might be a good investment if:

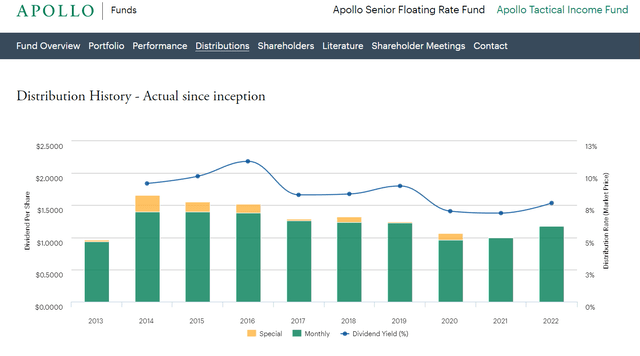

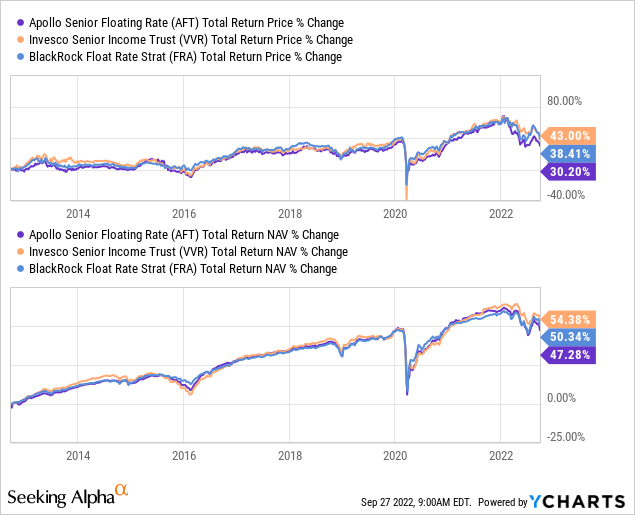

- You're looking for income. AFT typically pays a relatively high distribution yield. (That's the main reason why people invest in these things!).

- You're concerned about rising interest rates. The floating rate nature of the loans can provide a hedge against inflation.

- You're comfortable with some level of risk. Senior loans are not risk-free, and leverage can amplify those risks.

- You understand the complexities of closed-end funds and senior loan investing. (Do your homework!).

AFT might NOT be a good investment if:

- You're risk-averse. (Stick to CDs or Treasury bonds!).

- You need easy access to your money. (Closed-end funds are not as liquid as some other investments).

- You don't understand the risks involved. (Seriously, don't invest in something you don't understand!).

- You're looking for rapid growth. (Income is the primary focus here, not capital appreciation).

Final Thoughts

The Apollo Senior Floating Rate Fund Inc. is a complex investment vehicle that offers the potential for income and inflation protection. However, it also comes with its share of risks. Before investing in AFT, it's essential to do your own research, understand the risks involved, and consider your own investment goals and risk tolerance. And maybe, just maybe, consult with a financial advisor. (They're the professionals, after all!).

As for Dave, my burger-loving neighbor? Well, he's still happily invested in AFT (as far as I know). And, hopefully, his burgers are turning out a bit better than mine!

Remember, I'm just some random person on the internet, so this isn't financial advice! Do your own research and make informed decisions!