Accrued Interest Paid On Purchases 1099

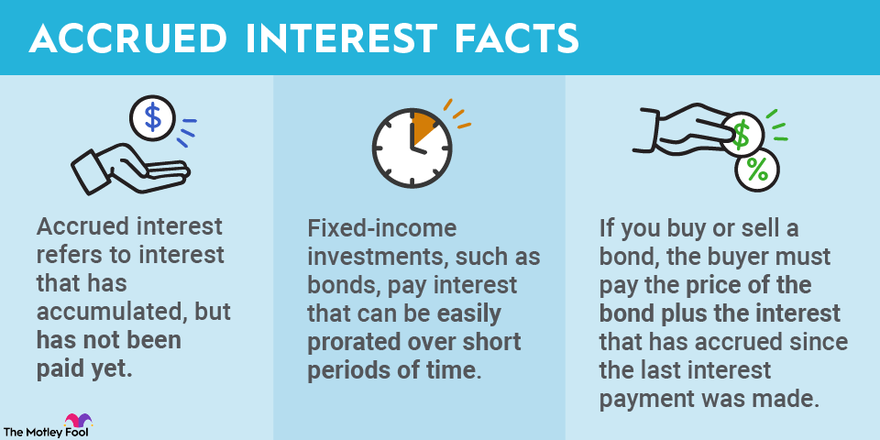

Accrued interest paid on purchases, particularly in the context of bond transactions, represents a nuanced area of financial reporting that often requires careful attention to detail. This arises because bond sales rarely coincide precisely with interest payment dates. When a bond is sold between these dates, the buyer compensates the seller for the interest that has accrued since the last payment. This amount, though seemingly straightforward, has implications for both the buyer and seller, and necessitates accurate reporting on Form 1099-INT.

Causes of Accrued Interest

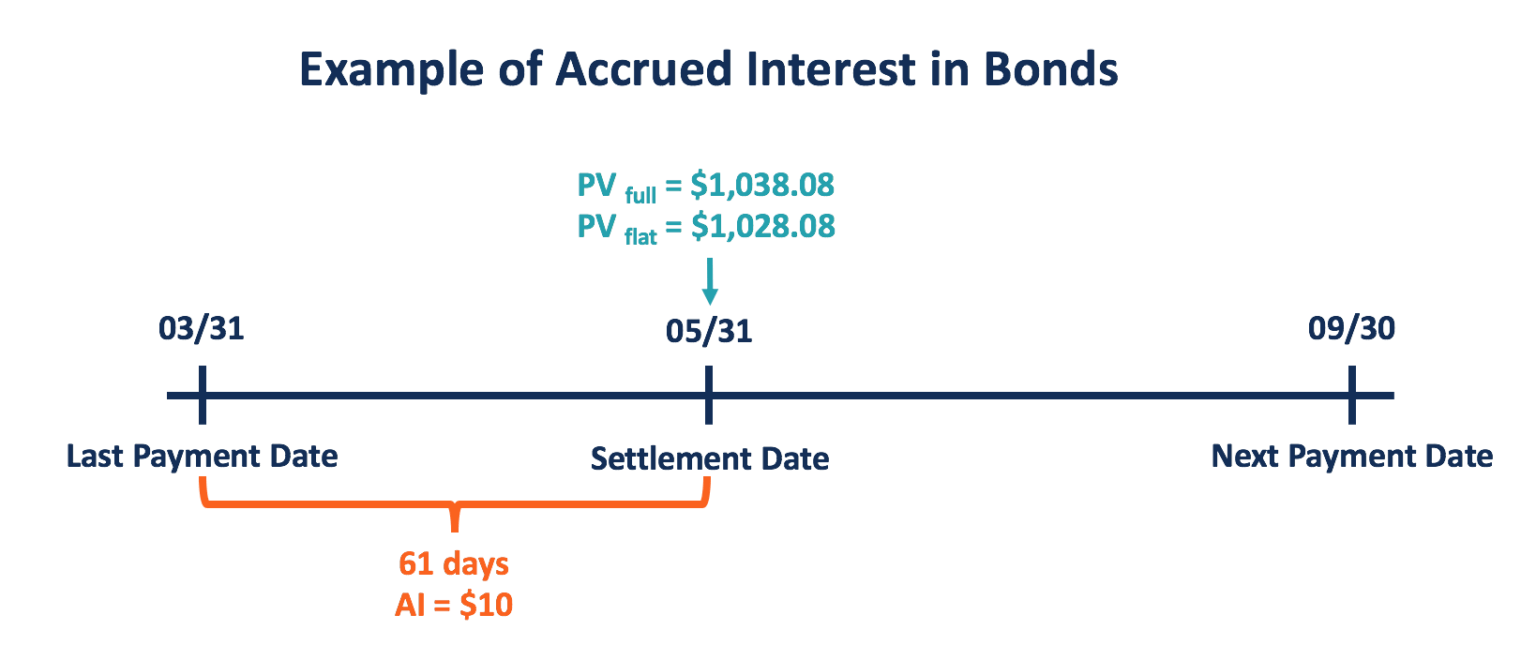

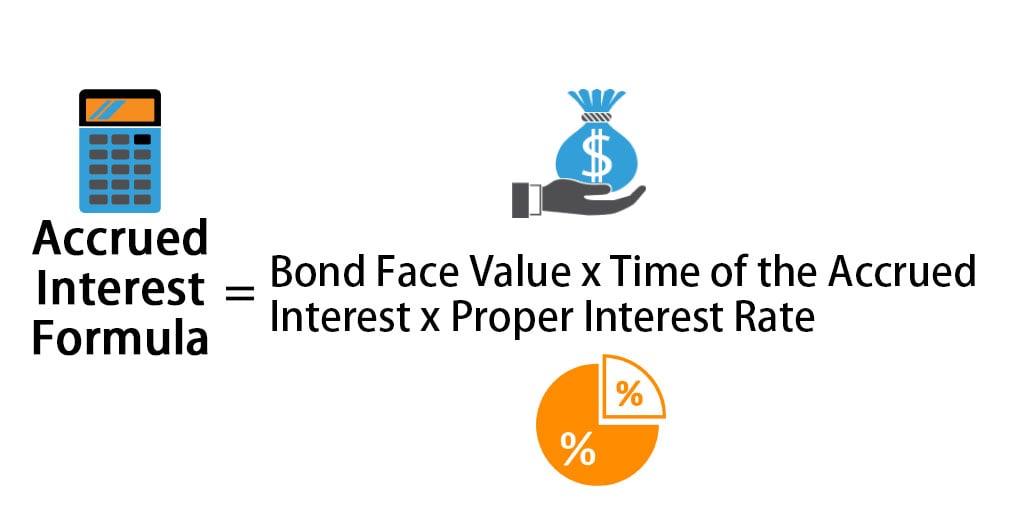

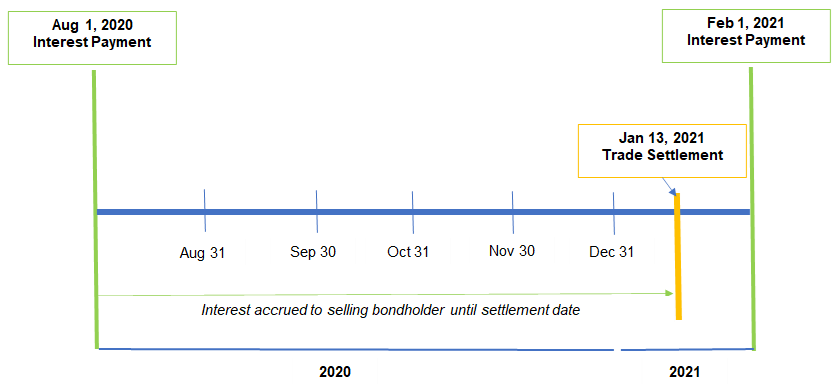

The fundamental cause of accrued interest stems from the periodic nature of interest payments on debt instruments. Bonds, for example, typically pay interest semi-annually. Unless a bond is bought or sold exactly on those payment dates, some interest will have accrued. The seller has held the bond for a portion of the period and is entitled to the corresponding interest earned during that time. To compensate the seller, the buyer pays the market price of the bond plus the accrued interest. This mechanism ensures that the seller receives the full economic benefit of holding the bond up to the point of sale.

Market dynamics also play a role. The constant buying and selling of bonds means that transactions are happening continuously, regardless of interest payment schedules. This constant trading activity necessitates a way to fairly allocate the interest earned, hence the convention of paying accrued interest.

Must Read

Another contributing factor is standardization within the financial industry. The practice of accrued interest simplifies the accounting process for both buyers and sellers. Without it, determining the true economic gain or loss on a bond transaction would be far more complex.

Effects of Accrued Interest on Buyers and Sellers

The effects of accrued interest differ for the buyer and seller of the bond.

For the Seller:

The seller receives cash for the bond’s market price and the accrued interest. However, the accrued interest portion is considered interest income, and is therefore taxable. This is a crucial point, as the seller must report this interest income on their tax return. The 1099-INT form serves as the official documentation of this income.

![How to Report Interest Income to IRS [Form 1040] | Serving Those Who Serve](https://stwserve.com/wp-content/uploads/2024/03/Picture1-1099-INT.png)

Because the seller receives the accrued interest, it effectively offsets the interest income that will be reflected on the next interest payment date. The seller is only taxed on the interest they have actually earned by holding the bond.

For the Buyer:

The buyer pays the market price of the bond plus the accrued interest. This payment represents a reduction in the interest income they will receive on the next interest payment date. When the next interest payment arrives, the buyer will receive the full interest payment, but a portion of that will represent a return of the accrued interest they paid at the time of purchase. This portion is not taxable. It’s considered a return of capital, not income.

Essentially, the buyer is pre-paying a portion of the next interest payment. The amount of the pre-payment is equal to the accrued interest owed to the seller. For tax purposes, the buyer treats this pre-payment as a reduction of interest income when they receive the next full payment. They are only taxed on the net amount of interest earned during their ownership period.

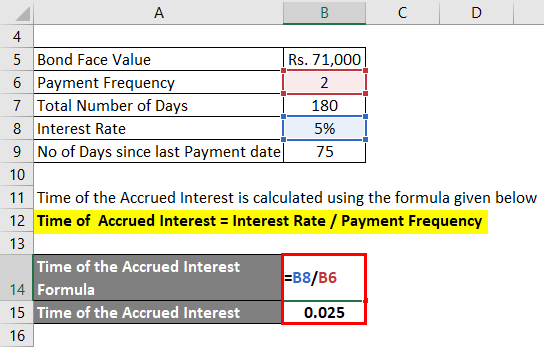

Consider a simple example: Suppose a bond pays $100 in semi-annual interest. If a buyer purchases the bond halfway through the period, they will pay the seller $50 in accrued interest. When the next interest payment arrives, the buyer will receive the full $100. However, they will only be taxed on $50, because $50 was a return of the pre-payment.

Implications for Form 1099-INT Reporting

Form 1099-INT, Interest Income, is the document used to report interest income to the IRS and to taxpayers. When accrued interest is involved in a bond transaction, it impacts the information reported on this form.

For the seller, the broker or financial institution will typically include the accrued interest portion in box 1 of Form 1099-INT, labeled "Interest income." The seller is responsible for reporting this amount as taxable income.

For the buyer, the situation is more complex. The 1099-INT they receive will report the gross interest income received, without factoring in the accrued interest they initially paid. It is the buyer's responsibility to make the necessary adjustments on their tax return to account for the accrued interest. This often involves tracking the accrued interest paid and subtracting it from the gross interest received as reported on the 1099-INT.

The IRS provides guidance on how to handle accrued interest in Publication 550, Investment Income and Expenses. This publication outlines the rules for both buyers and sellers and provides examples of how to calculate and report accrued interest for tax purposes.

Accurate reporting of accrued interest is critical to avoid tax discrepancies and potential penalties. Failure to properly account for accrued interest can lead to an overpayment or underpayment of taxes, which can trigger an audit or require amended tax returns.

It's important to note that brokerages and financial institutions do not always explicitly identify the accrued interest amount on the transaction confirmation or on the 1099-INT form. Therefore, it's often the taxpayer's responsibility to track this information diligently and consult with a tax professional if needed.

Data from the IRS indicates that errors related to investment income, including interest income, are a common source of tax filing mistakes. Proper understanding and application of the rules regarding accrued interest can significantly reduce the risk of such errors.

:max_bytes(150000):strip_icc()/ScreenShot2020-02-03at11.47.45AM-80a4044783b44a7b85412e8cd21bcbbc.png)

Broader Significance

The concept of accrued interest paid on purchases, while seemingly a niche topic, highlights the importance of understanding the underlying economics of financial transactions. It demonstrates the need for fair allocation of economic benefits and the careful tracking of financial flows. The accrued interest mechanism ensures that neither the buyer nor the seller is unfairly advantaged or disadvantaged by the timing of a transaction.

Moreover, the accurate reporting of accrued interest underscores the broader importance of tax compliance and the responsibility of taxpayers to understand and adhere to the relevant tax laws. The complexity surrounding accrued interest also underscores the value of seeking professional advice when navigating complex financial transactions.

In a world increasingly reliant on complex financial instruments and rapidly changing markets, the principle of accrued interest serves as a reminder that even seemingly small details can have significant financial and tax implications. Ignoring these details can lead to unintended consequences, whereas careful attention to them can ensure fair and accurate financial reporting.

Finally, the treatment of accrued interest serves as a microcosm of broader principles in accounting and finance, emphasizing the importance of accrual accounting (recognizing revenues and expenses when earned or incurred, regardless of when cash changes hands) and the time value of money. By understanding the mechanics of accrued interest, investors gain a deeper appreciation for the complexities and nuances of the financial markets and the importance of diligent record-keeping and tax planning.

:max_bytes(150000):strip_icc()/accured-interest-fa7c00af884947a7a32cd1daa57c3462.jpg)