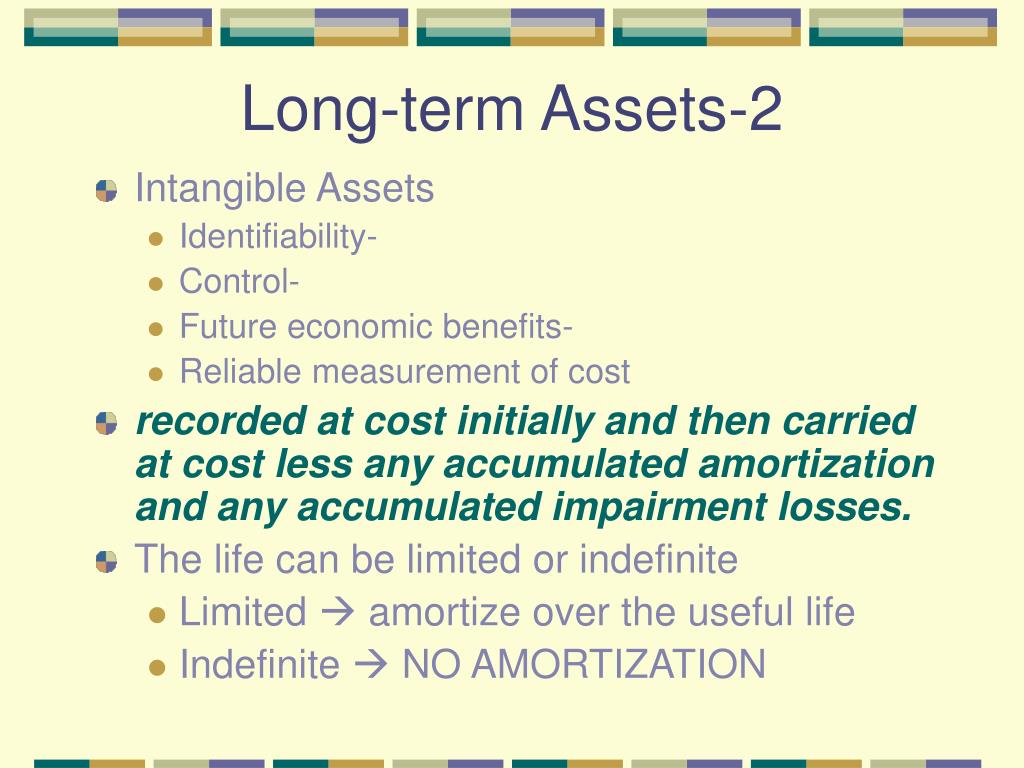

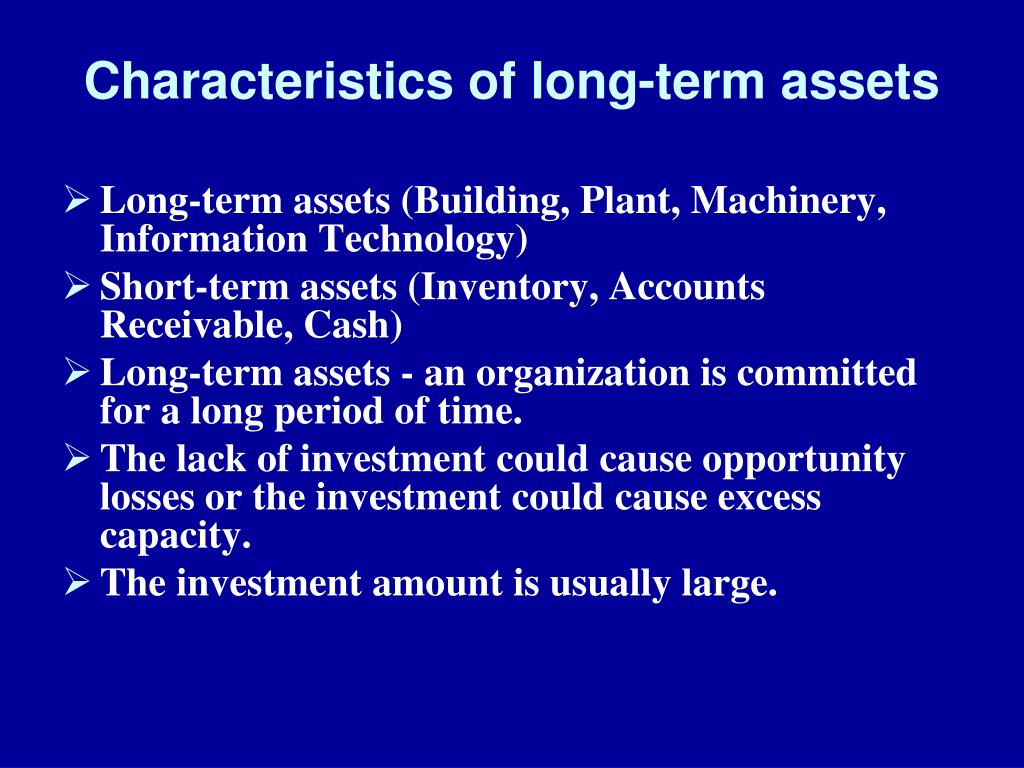

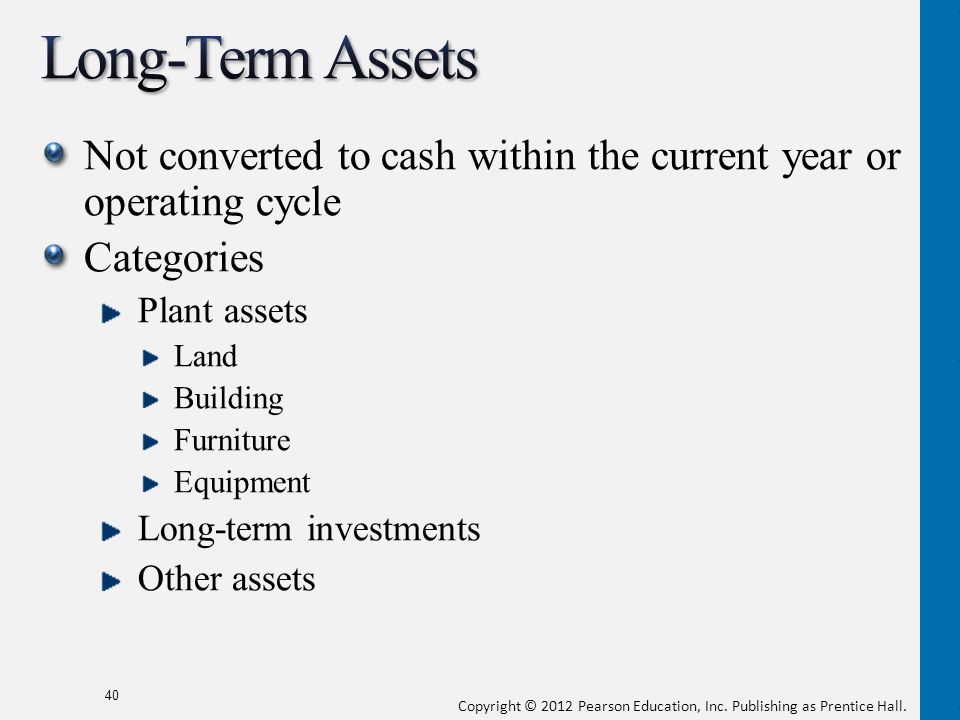

A Long-term Asset Is Recorded At The

The recording of long-term assets forms the bedrock of a company's financial health, profoundly impacting its balance sheet and subsequent financial performance. However, the seemingly straightforward act of recording these assets can become a complex exercise with significant consequences depending on the valuation method and accounting policies employed. This analysis explores the nuances of recording long-term assets, dissecting the causes, effects, and broader implications stemming from the initial recording process.

Causes Influencing the Initial Recording of Long-Term Assets

Several factors coalesce to influence how a long-term asset is initially recorded. These factors can be broadly categorized as regulatory, market-driven, and management-influenced.

Regulatory Frameworks

The accounting standards established by bodies like the Financial Accounting Standards Board (FASB) in the United States and the International Accounting Standards Board (IASB) globally dictate the permissible methods for valuing and recording long-term assets. These standards, such as those related to property, plant, and equipment (PP&E) and intangible assets, provide a framework that aims to ensure consistency and comparability across financial statements. For instance, IFRS often allows for revaluation of certain assets, whereas U.S. GAAP historically relies more heavily on historical cost. This foundational regulatory difference impacts the initial recording value and subsequent depreciation or amortization.

Must Read

Market Conditions

Prevailing market conditions at the time of acquisition play a pivotal role. If an asset is acquired during a period of high inflation, its recorded cost, even if reflecting fair market value at that time, might appear inflated compared to assets acquired during periods of economic stability. Conversely, during economic downturns, acquiring assets at depressed prices can lead to an undervalued initial recording, potentially misrepresenting the asset's long-term productive capacity. For example, the acquisition of real estate during the 2008 financial crisis often resulted in assets being recorded at significantly lower values than their pre-crisis worth, creating a potential for future gains as the market recovered.

Management Discretion and Intent

Management teams exercise considerable discretion in applying accounting standards. Choices around capitalization policies, depreciation methods (e.g., straight-line, declining balance), and estimations of useful lives significantly impact the initial recording and subsequent expense recognition. Aggressive capitalization policies, where costs that could be expensed are instead capitalized as part of the asset's value, can artificially inflate the asset's recorded value and boost short-term profitability. Similarly, choosing longer useful lives for depreciation reduces the annual depreciation expense, again improving near-term earnings. These choices, while often technically permissible within the bounds of accounting standards, can have profound effects on the perceived financial health of the company. Consider the airline industry; choosing longer depreciable lives for aircraft can significantly reduce annual expenses, but it also might understate the actual cost of operating the fleet.

Effects of the Initial Recording Value

The initial recording value of a long-term asset reverberates through the financial statements, influencing profitability, solvency, and investor perceptions.

Impact on Profitability

The initial recording directly affects future depreciation or amortization expenses. A higher initial value leads to higher annual expenses, reducing net income and potentially impacting earnings per share. Conversely, a lower initial value reduces these expenses, boosting profitability. Consider a software company capitalizing development costs as an intangible asset. A generous definition of "development" could significantly increase the value of the asset, reducing immediate R&D expenses but increasing future amortization charges. The timing of these charges can significantly alter the company's reported earnings trajectory.

Influence on Solvency Ratios

The recording of long-term assets impacts solvency ratios such as debt-to-assets. Inflated asset values can improve these ratios, making the company appear less risky to creditors and investors. However, this improved solvency might be illusory if the asset's true value is significantly lower.

For instance, if a company overvalues its real estate holdings, its debt-to-asset ratio will appear healthier, potentially enabling it to secure more favorable loan terms. However, if the real estate market declines, the overstated asset value could mask underlying financial distress.

Investor Perception and Market Valuation

Investors rely on financial statements to assess a company's value and future prospects. The initial recording of long-term assets can significantly influence these perceptions. Overstated asset values can create a false sense of security and attract investors, leading to inflated stock prices. Conversely, understated asset values might lead to undervaluation, potentially making the company a target for acquisition or limiting its access to capital. The Enron scandal provides a stark reminder of the consequences of manipulating asset values to deceive investors. Their aggressive accounting practices, including the misrepresentation of asset values, ultimately led to the company's downfall.

:max_bytes(150000):strip_icc()/Longtermassets_final-633c56a416364f9a96654d4a5f3a73cc.png)

Implications and Broader Significance

The implications of how long-term assets are recorded extend beyond the immediate financial statements, influencing economic activity, resource allocation, and overall market efficiency.

Impact on Resource Allocation

Inaccurate recording of asset values can distort resource allocation within a company. If assets are overvalued, management might allocate excessive resources to maintaining or expanding operations related to those assets, even if they are not generating sufficient returns. This misallocation can hinder investment in more profitable ventures and ultimately harm the company's long-term competitiveness. Conversely, undervaluation can lead to underinvestment in potentially valuable assets, stifling growth opportunities. A manufacturing company that undervalues its machinery might postpone necessary upgrades, leading to decreased productivity and ultimately a loss of market share.

Effects on Corporate Governance

The process of recording long-term assets highlights the importance of strong corporate governance and ethical leadership. Management teams must exercise integrity and objectivity in applying accounting standards, ensuring that asset values are fairly represented. Independent audit committees play a crucial role in overseeing the recording process and challenging management's assumptions. Failures in corporate governance, such as those seen in companies like WorldCom, often involve manipulation of asset values to inflate profits and conceal underlying financial problems. A robust internal control environment and independent audits are essential safeguards against such manipulation.

Macroeconomic Implications

At a macroeconomic level, widespread misreporting of asset values can contribute to financial instability. Inflated asset values can fuel speculative bubbles, leading to unsustainable economic growth followed by painful corrections. The housing bubble of the mid-2000s, fueled in part by lax lending standards and inflated appraisals of real estate, provides a cautionary tale of the macroeconomic consequences of distorted asset values. Accurate and transparent reporting of long-term assets is therefore crucial for maintaining the stability and efficiency of the financial system.

In conclusion, the initial recording of a long-term asset is far from a simple bookkeeping entry; it's a pivotal decision with far-reaching consequences. The interplay of regulatory frameworks, market conditions, and management discretion shapes the recorded value, influencing profitability, solvency, investor perceptions, and ultimately, the allocation of resources. The integrity and transparency with which long-term assets are recorded are not merely accounting technicalities but fundamental pillars supporting corporate governance, market efficiency, and broader economic stability. The long-term implications of these initial choices demand diligent oversight, ethical leadership, and a commitment to fair and accurate financial reporting.

.jpg)