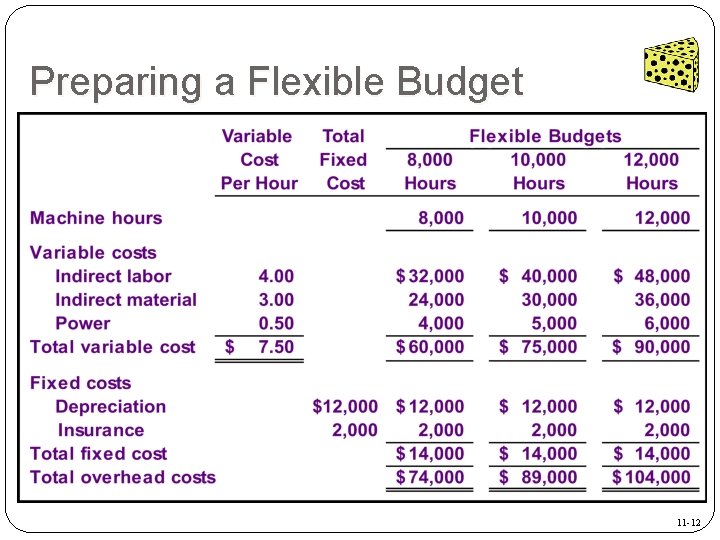

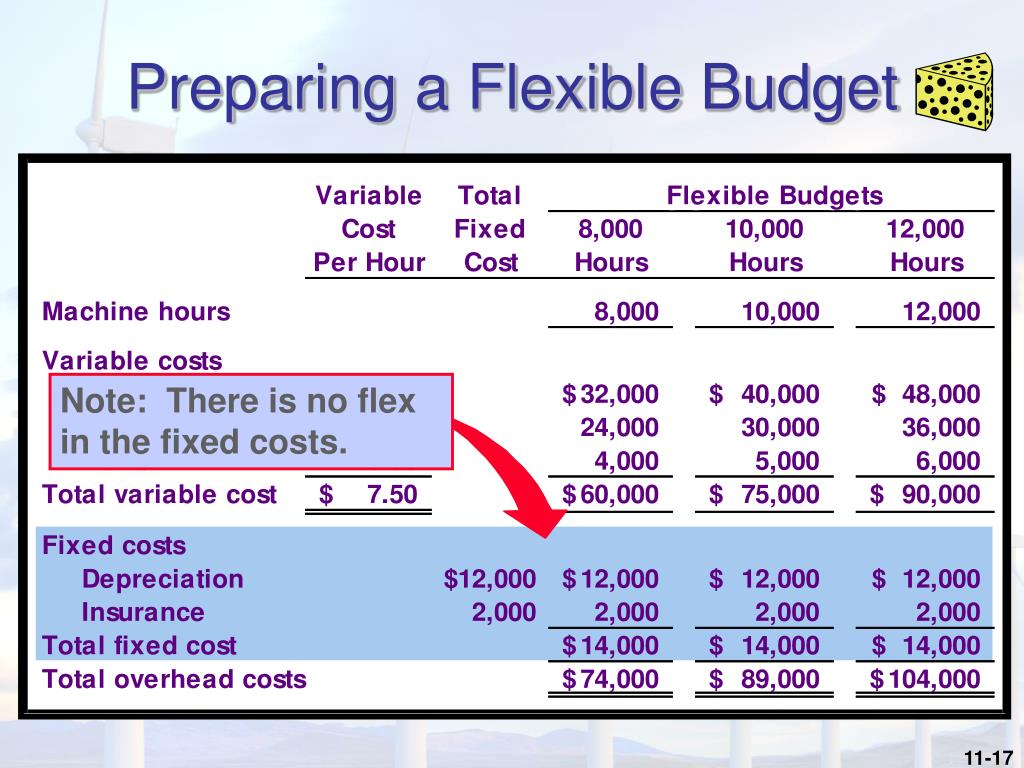

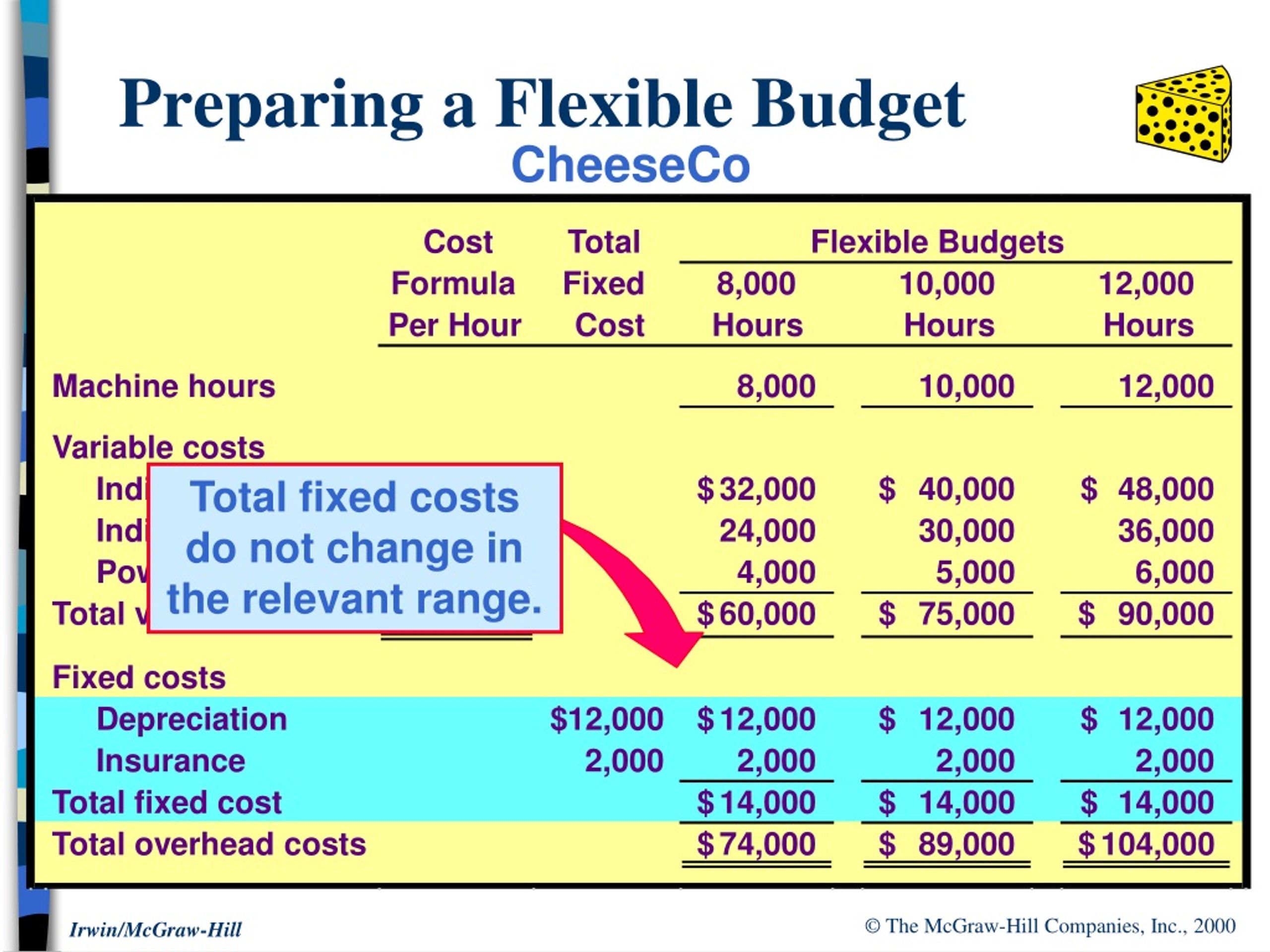

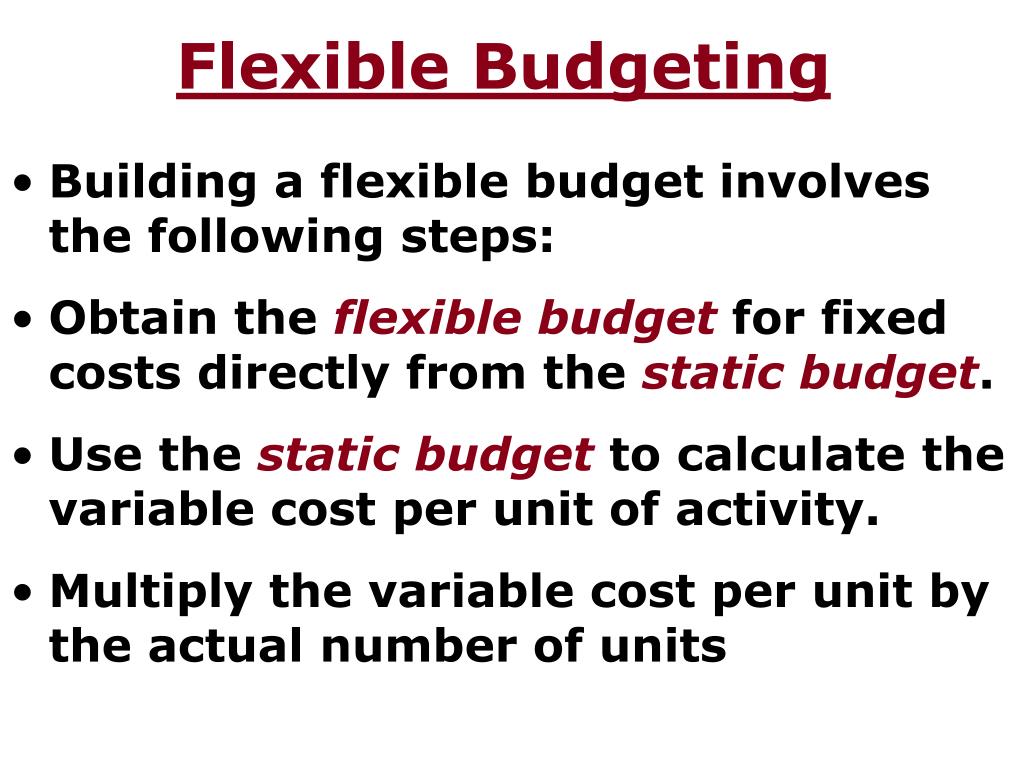

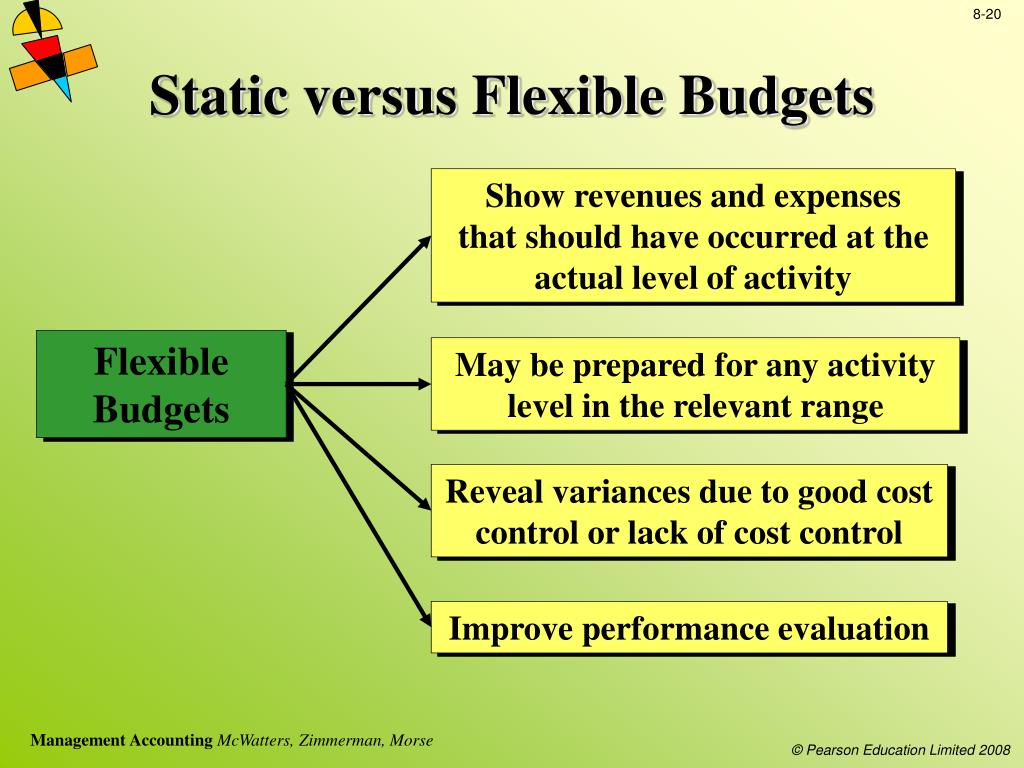

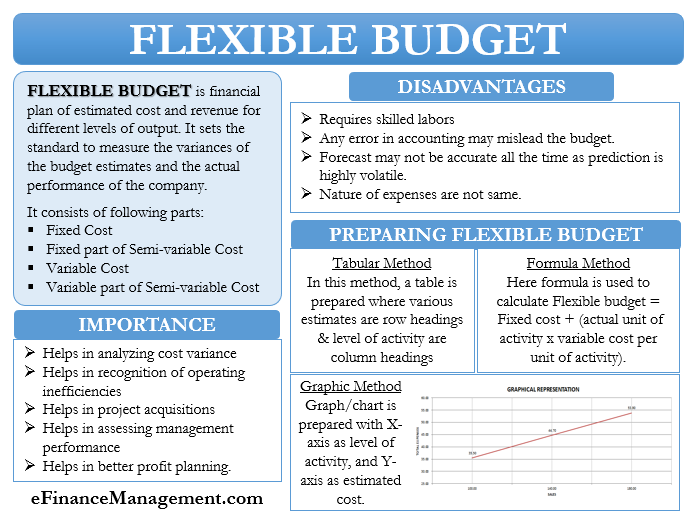

A Flexible Budget May Be Prepared:

A flexible budget represents a cornerstone of effective managerial accounting, offering a dynamic approach to financial planning and performance evaluation. Unlike a static budget, which remains fixed regardless of actual activity levels, a flexible budget adjusts to reflect the actual volume of production or sales achieved. This adaptability stems from its construction based on cost behavior patterns, separating fixed costs (which remain constant irrespective of activity) from variable costs (which fluctuate proportionally with activity). The ability to prepare a flexible budget is not merely a technical accounting exercise; it has profound causes, far-reaching effects, and significant implications for organizational strategy and operational efficiency.

Causes Leading to the Preparation of Flexible Budgets

The primary driver behind the adoption of flexible budgeting lies in the inherent limitations of static budgets. Static budgets, while useful for initial planning, become quickly irrelevant when actual activity deviates from the planned level. For instance, if a company budgets for sales of 10,000 units but only sells 8,000, comparing actual costs against the static budget will inevitably lead to unfavorable variances. These variances, however, may not accurately reflect managerial performance. They could simply be a result of the lower sales volume. This inadequacy spurred the development and implementation of flexible budgets. According to the Institute of Management Accountants (IMA), approximately 70% of companies use some form of flexible budgeting in their operations, highlighting its widespread acceptance as a superior tool for variance analysis and performance evaluation. This percentage has steadily increased over the past two decades, reflecting a growing awareness of its benefits.

A key cause is the increasing complexity of business environments. Globalization, technological advancements, and volatile market conditions demand greater agility and responsiveness from organizations. Companies are constantly faced with unforeseen fluctuations in demand, supply chain disruptions, and competitive pressures. A flexible budget provides a framework for quickly adapting to these changes and understanding their financial impact. Consider a manufacturing firm that relies on imported raw materials. If exchange rates unexpectedly shift, a flexible budget can be easily adjusted to reflect the altered cost of materials, allowing management to make informed decisions about pricing and production levels.

Must Read

Furthermore, the rise of data analytics and enterprise resource planning (ERP) systems has facilitated the preparation of flexible budgets. ERP systems provide real-time data on activity levels and costs, making it easier to track actual performance and adjust the budget accordingly. Data analytics tools enable businesses to identify cost behavior patterns and develop accurate cost formulas, which are essential for constructing a reliable flexible budget. The accessibility of these technologies has democratized the use of flexible budgeting, making it feasible for even smaller organizations to implement. This is particularly evident in industries with high operating leverage, such as airlines and hotels, where even small changes in occupancy rates can have a significant impact on profitability.

Effects of Implementing Flexible Budgets

The implementation of flexible budgets has a multitude of positive effects on organizational performance. One of the most significant effects is improved variance analysis. By comparing actual costs against the flexible budget, management can isolate variances that are truly attributable to inefficiencies or effective cost control. This allows for a more accurate assessment of managerial performance and facilitates targeted corrective actions. For example, if a company incurs a favorable labor cost variance under a static budget, it may be tempted to praise the efficiency of its workforce. However, a flexible budget may reveal that the favorable variance is simply due to lower-than-expected production volume, masking underlying inefficiencies in labor productivity.

Flexible budgets also promote better cost control. By understanding how costs change with activity levels, management can identify areas where costs can be reduced or optimized. For instance, a flexible budget may reveal that certain overhead costs are not truly fixed and are, in fact, partially variable. This insight can lead to the implementation of strategies to better manage these costs and improve profitability. A 2021 study by the consulting firm Deloitte found that companies using flexible budgeting experienced a 5-10% improvement in cost control compared to those relying solely on static budgets.

Moreover, flexible budgets enhance decision-making. They provide management with a more realistic view of the financial consequences of different operating decisions. For example, if a company is considering accepting a special order at a lower price, a flexible budget can be used to estimate the incremental costs and revenues associated with the order, allowing management to make an informed decision about whether to accept it. This is particularly relevant in situations where capacity is constrained or when negotiating pricing with large customers. The ability to quickly model different scenarios based on varying activity levels is a key advantage of flexible budgeting.

Flexible budgets also contribute to more accurate forecasting. By analyzing historical data on cost behavior and activity levels, management can develop more reliable forecasts of future performance. This improved forecasting can lead to better resource allocation, more effective pricing strategies, and improved profitability.

Implications of Flexible Budgeting

The implications of flexible budgeting extend beyond internal financial management and have significant ramifications for organizational strategy and stakeholder relations. A key implication is its contribution to strategic alignment. Flexible budgeting allows organizations to link their financial plans more closely to their operational goals. By understanding how costs respond to changes in activity, companies can make more informed decisions about resource allocation, pricing, and product mix, ensuring that their financial plans support their overall strategic objectives. This alignment is crucial for achieving sustainable competitive advantage.

Another important implication is its impact on stakeholder confidence. Investors, creditors, and other stakeholders rely on financial information to assess the performance and prospects of an organization. A company that uses flexible budgeting demonstrates a commitment to transparency and accountability, enhancing stakeholder confidence in its financial reporting. The ability to explain variances and provide a clear understanding of how costs respond to changes in activity builds trust and credibility with external stakeholders.

Flexible budgeting also has implications for organizational culture. By promoting a data-driven approach to decision-making, it can foster a culture of continuous improvement and accountability. When employees understand how their actions impact costs and profitability, they are more likely to be engaged in efforts to improve efficiency and reduce waste. This can lead to a more productive and motivated workforce.

However, the implementation of flexible budgeting is not without its challenges. It requires a significant investment in data collection and analysis. It also requires a thorough understanding of cost behavior patterns and the ability to develop accurate cost formulas. Furthermore, it may require changes to existing accounting systems and processes. Organizations must be prepared to address these challenges in order to fully realize the benefits of flexible budgeting. According to research from APQC, companies that successfully implement flexible budgeting typically invest in training and development programs to ensure that employees understand the principles and techniques involved.

Broader Significance

In conclusion, the ability to prepare a flexible budget represents a significant advancement in managerial accounting, offering a dynamic and responsive approach to financial planning and performance evaluation. Its causes are rooted in the limitations of static budgets and the increasing complexity of business environments. Its effects include improved variance analysis, better cost control, enhanced decision-making, and more accurate forecasting. Its implications extend beyond internal financial management, impacting strategic alignment, stakeholder confidence, and organizational culture. The broader significance of flexible budgeting lies in its ability to empower organizations to make more informed decisions, improve efficiency, and achieve sustainable competitive advantage. As business environments continue to evolve, the importance of flexible budgeting as a tool for effective management will only increase.