A Favorable Cost Variance Occurs When

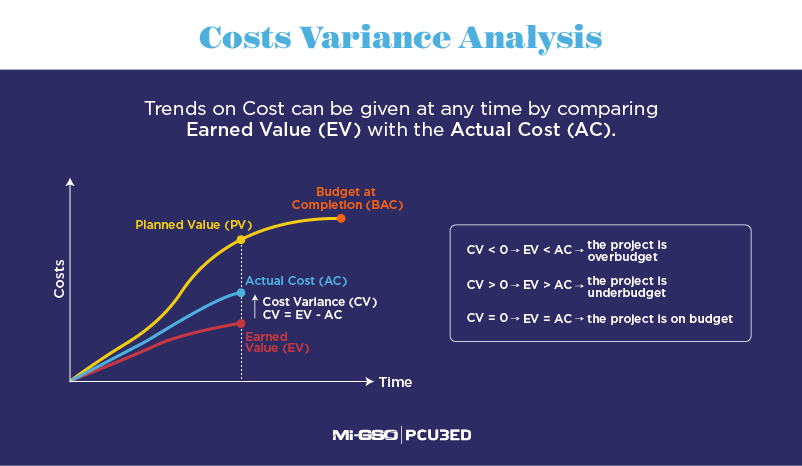

Cost variance is a crucial metric in managerial accounting, indicating the difference between the actual cost incurred and the standard cost expected for a particular activity or product. A favorable cost variance, specifically, signals that the actual costs were less than what was anticipated. Understanding when and why a favorable cost variance occurs is essential for effective cost management and decision-making.

Definition of Favorable Cost Variance

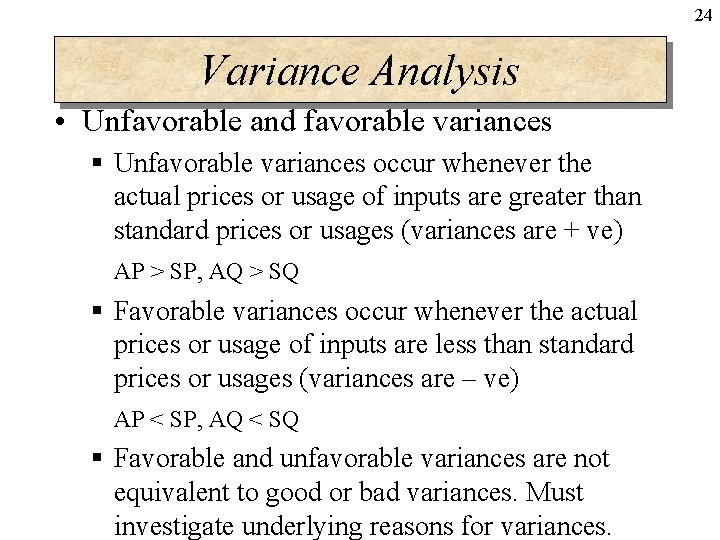

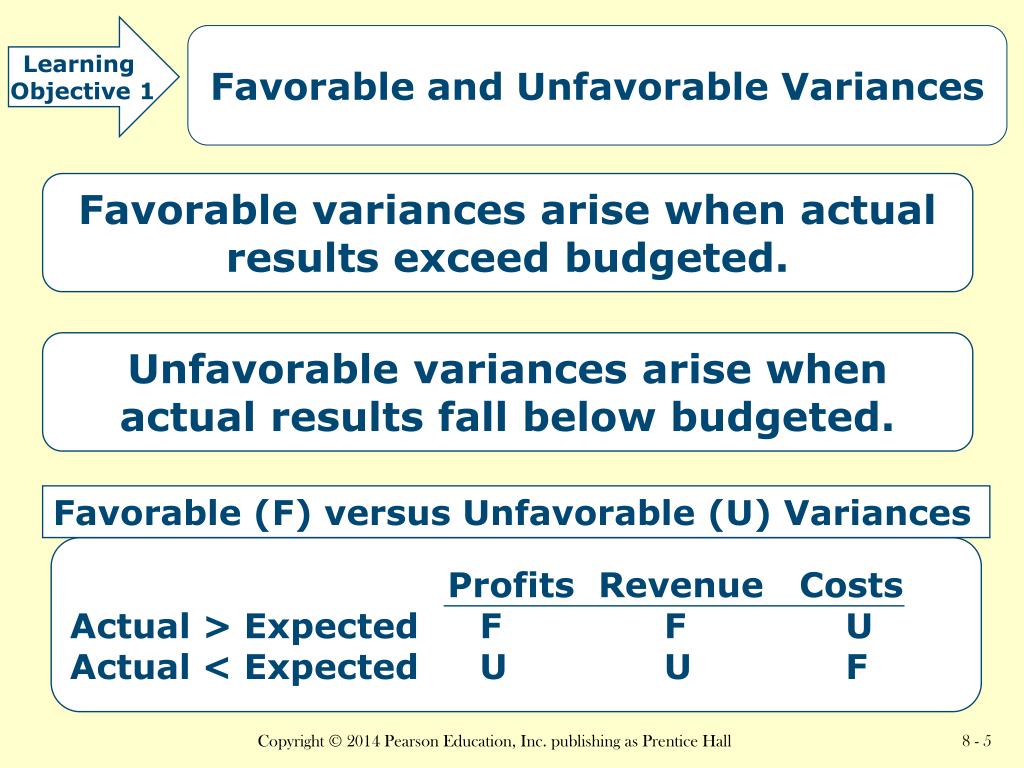

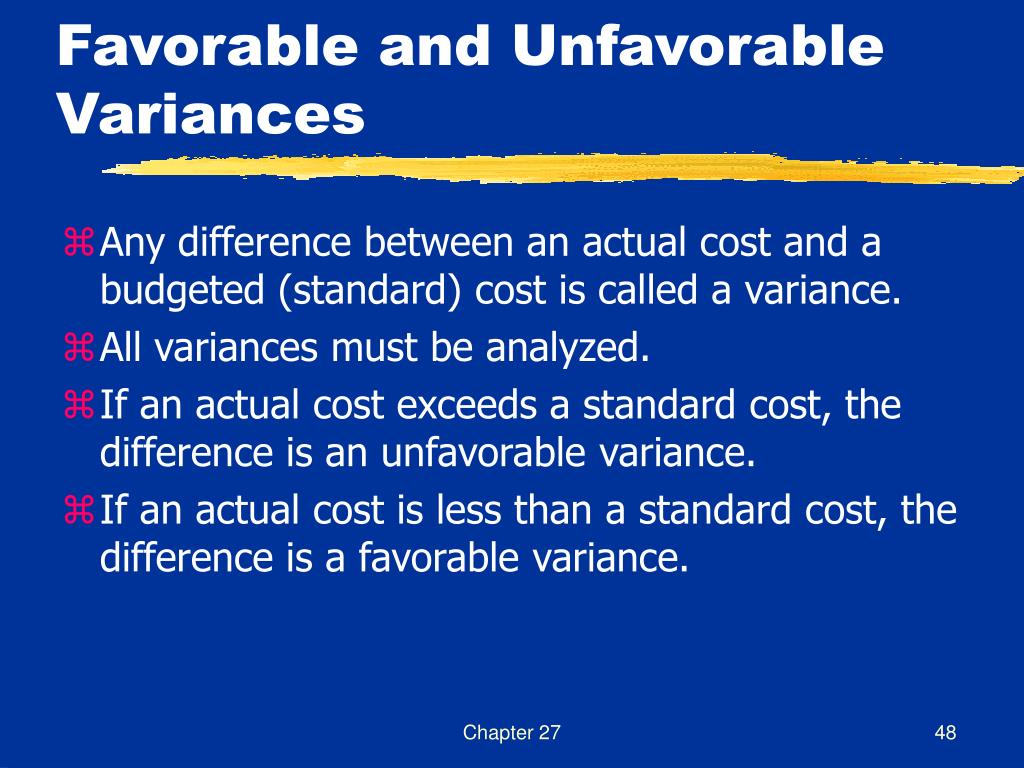

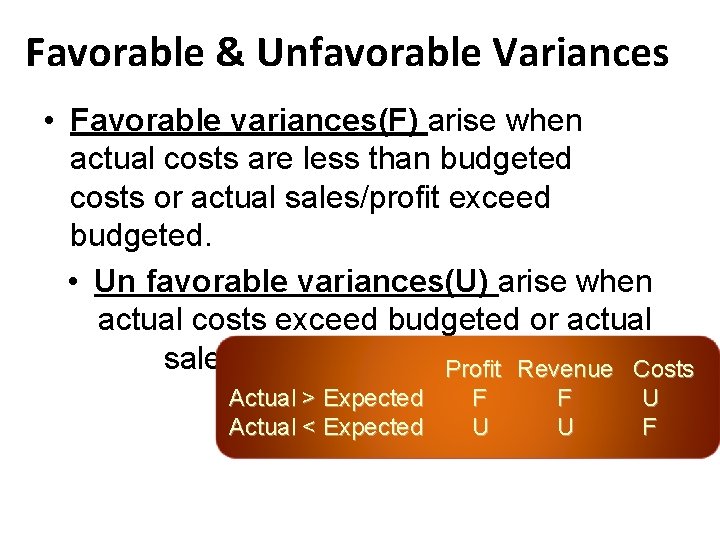

A favorable cost variance arises when the actual costs incurred are lower than the standard, or budgeted, costs. This indicates efficient operations, better negotiation with suppliers, or more productive use of resources than initially planned. Conversely, an unfavorable cost variance means the actual costs exceeded the standard costs.

The basic formula for calculating cost variance is:

Must Read

Cost Variance = Standard Cost - Actual Cost

If the result is positive, the variance is favorable. If the result is negative, the variance is unfavorable.

Situations Leading to Favorable Cost Variance

Several factors can contribute to a favorable cost variance. These generally fall into categories related to direct materials, direct labor, and overhead costs.

1. Direct Materials

A favorable direct materials cost variance occurs when the actual cost of materials used in production is less than the standard cost. This can be due to several reasons:

- Lower Purchase Price: The company may have negotiated better prices with suppliers, taken advantage of bulk discounts, or benefited from favorable market conditions leading to lower raw material costs. For example, if a company budgeted \$10 per unit for a raw material, but actually purchased it for \$8 per unit, this contributes to a favorable variance.

- Efficient Material Usage: Employees might have found ways to use materials more efficiently, reducing waste and spoilage. Training programs, improved equipment, or better process controls can all contribute. If the standard quantity of material per unit is 5 lbs, but the actual usage is 4.5 lbs, it is a favorable sign.

- Quality Improvements: Higher quality materials, despite potentially costing more per unit initially, may lead to less waste and fewer defects in the production process, ultimately reducing overall material costs.

- Strategic Sourcing: Discovering and utilizing alternative, lower-cost suppliers without sacrificing quality can significantly reduce material expenses.

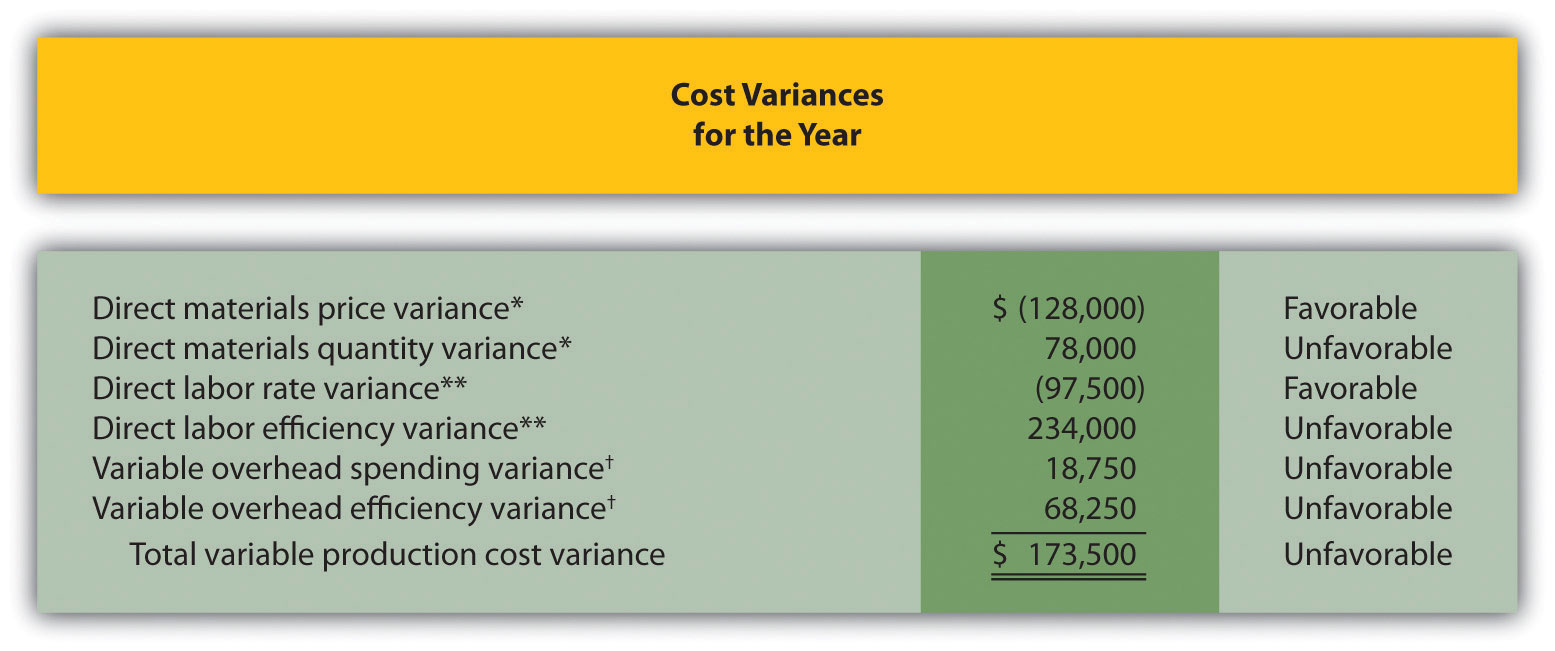

The Direct Materials Cost Variance can be further broken down into Direct Materials Price Variance and Direct Materials Quantity Variance. A favorable price variance indicates that the materials were purchased at a lower price than expected, while a favorable quantity variance means that less material was used than anticipated.

2. Direct Labor

A favorable direct labor cost variance occurs when the actual cost of labor used in production is less than the standard cost. This can be attributed to:

- Lower Wage Rates: The company may have been able to hire employees at lower wage rates than initially budgeted, or may have reduced overtime expenses. This is especially true if the labor market has shifted, making qualified employees more readily available at competitive wages.

- Increased Labor Efficiency: Employees might have become more proficient and productive due to training, experience, or improved work processes. For example, a new manufacturing technique might decrease the time required to complete a task.

- Improved Workforce Management: Effective scheduling and task assignment can optimize labor utilization and reduce idle time.

- Automation: Implementing automated systems can reduce the reliance on direct labor, potentially lowering labor costs significantly.

Similar to materials, the Direct Labor Cost Variance can be divided into Direct Labor Rate Variance and Direct Labor Efficiency Variance. A favorable rate variance signifies that labor was paid at a lower rate than expected, while a favorable efficiency variance implies that less labor time was used than planned.

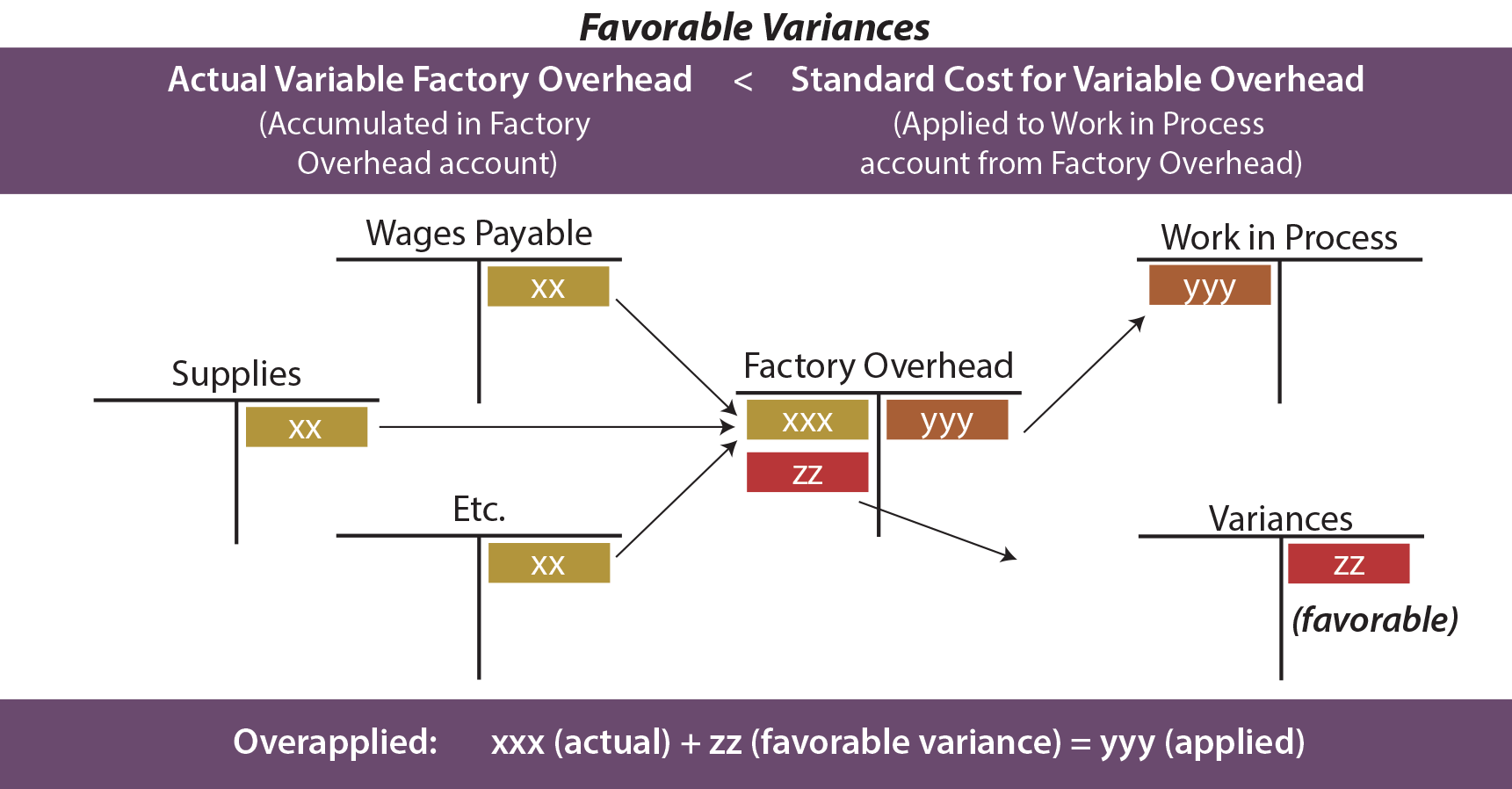

3. Overhead Costs

A favorable overhead cost variance occurs when the actual overhead costs are less than the standard overhead costs. Overhead costs encompass all indirect costs associated with production, such as factory rent, utilities, and indirect labor. Reasons for a favorable variance include:

- Effective Cost Control: Management's efforts to control and reduce overhead expenses, such as negotiating lower utility rates or reducing waste, can lead to a favorable variance.

- Increased Production Volume: If actual production volume exceeds the budgeted volume, fixed overhead costs are spread over a larger number of units, resulting in a lower overhead cost per unit.

- Accurate Budgeting: More accurate budgeting processes can prevent overestimation of overhead costs in the initial budget.

- Negotiated Discounts: Securing discounts on services like insurance or maintenance can contribute to lower overhead costs.

Overhead cost variances are typically analyzed as variable overhead variance and fixed overhead variance. A favorable variable overhead variance implies that variable overhead costs were lower than expected, given the actual level of activity. A favorable fixed overhead variance suggests that fixed overhead costs were lower than budgeted.

Interpreting and Responding to Favorable Cost Variances

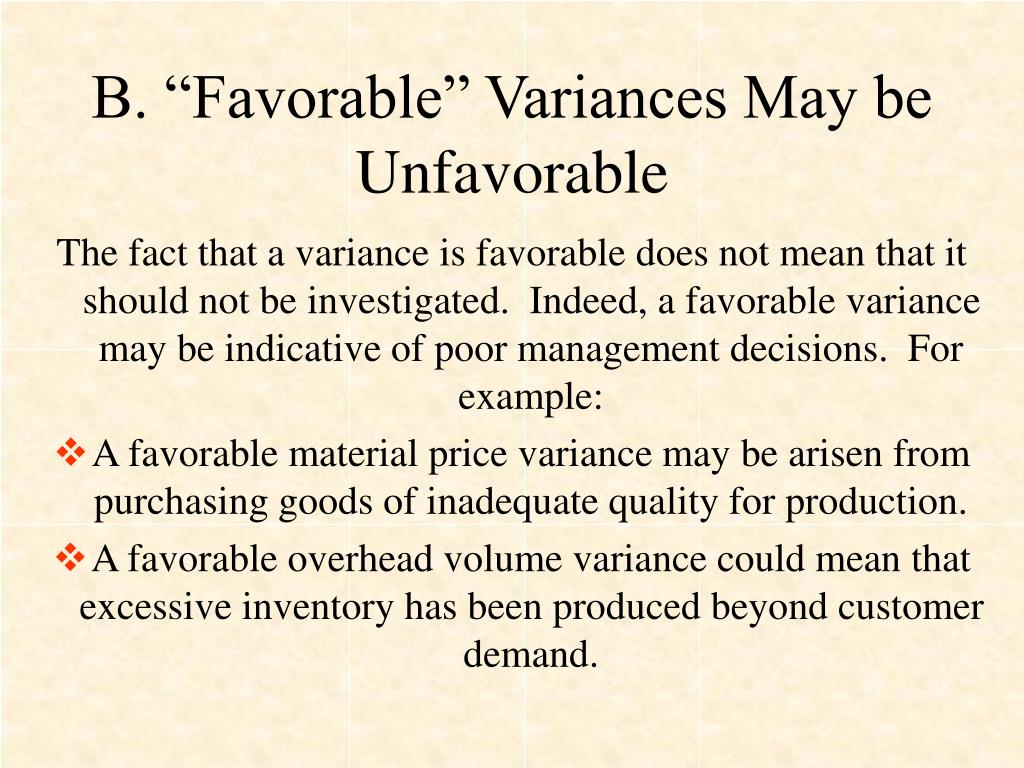

While a favorable cost variance generally indicates positive performance, it's crucial to investigate the underlying causes thoroughly. A favorable variance should not automatically be celebrated without understanding why it occurred. Some potential pitfalls include:

..jpg)

- Compromised Quality: A lower material cost may have been achieved by using cheaper, lower-quality materials, which could lead to product defects and customer dissatisfaction in the long run.

- Unsustainable Practices: Labor cost reductions may have been achieved through unsustainable practices, such as excessive employee workloads or unsafe working conditions, leading to higher turnover and potential legal issues.

- Inaccurate Standards: The standard costs used for comparison may have been inaccurate or outdated. A favorable variance might simply indicate that the original standards were too high, rather than representing genuine cost savings.

Therefore, companies should:

- Investigate the Root Causes: Determine the specific factors that contributed to the favorable variance.

- Assess the Impact on Quality and Other Areas: Evaluate whether the cost savings came at the expense of quality, employee morale, or other important aspects of the business.

- Adjust Future Standards: If the favorable variance is due to inaccurate standards, revise the standards to reflect more realistic expectations.

- Share Best Practices: If the favorable variance is a result of improved efficiency or innovative practices, share these practices across the organization to replicate the success.

Practical Advice and Insights

The principles of cost variance analysis can be applied beyond the realm of business to personal finance and everyday life. Here's how:

- Budgeting and Tracking Expenses: Create a budget and track your actual spending against it. A favorable variance means you've spent less than anticipated in a specific category (e.g., groceries, entertainment).

- Negotiating Prices: When making purchases, negotiate for better deals or compare prices from different vendors. A favorable variance is achieved when you secure a lower price than you initially expected.

- Efficient Resource Usage: Be mindful of your consumption of resources such as electricity, water, and fuel. Reducing your usage below your usual level results in a favorable variance in your utility bills.

- Home Improvement Projects: Before undertaking a home improvement project, create a detailed budget. A favorable cost variance means you completed the project for less than your estimated cost.

By understanding the concept of favorable cost variance and applying it in both professional and personal settings, you can make more informed decisions, improve efficiency, and achieve your financial goals. It's about being proactive, monitoring performance, and continuously seeking ways to optimize resource utilization.