$6 000 A Month Is How Much A Year

Okay, so picture this: I'm at my favorite café, sipping a latte that probably cost more than my first car payment (slight exaggeration, maybe...okay, huge exaggeration). My friend, let’s call him… Reginald (because why not?), leans in conspiratorially. "Dude," he whispers, "I heard someone makes $6,000 a month. How much is that a year? Is that, like, rich people money?"

My first instinct was to dramatically spit out my latte. But, you know, manners. Plus, I needed that caffeine. Instead, I calmly said, "Reginald, my friend, let's do some basic math. Prepare to be amazed...or mildly interested, at the very least."

The Big Reveal (It's Not That Dramatic)

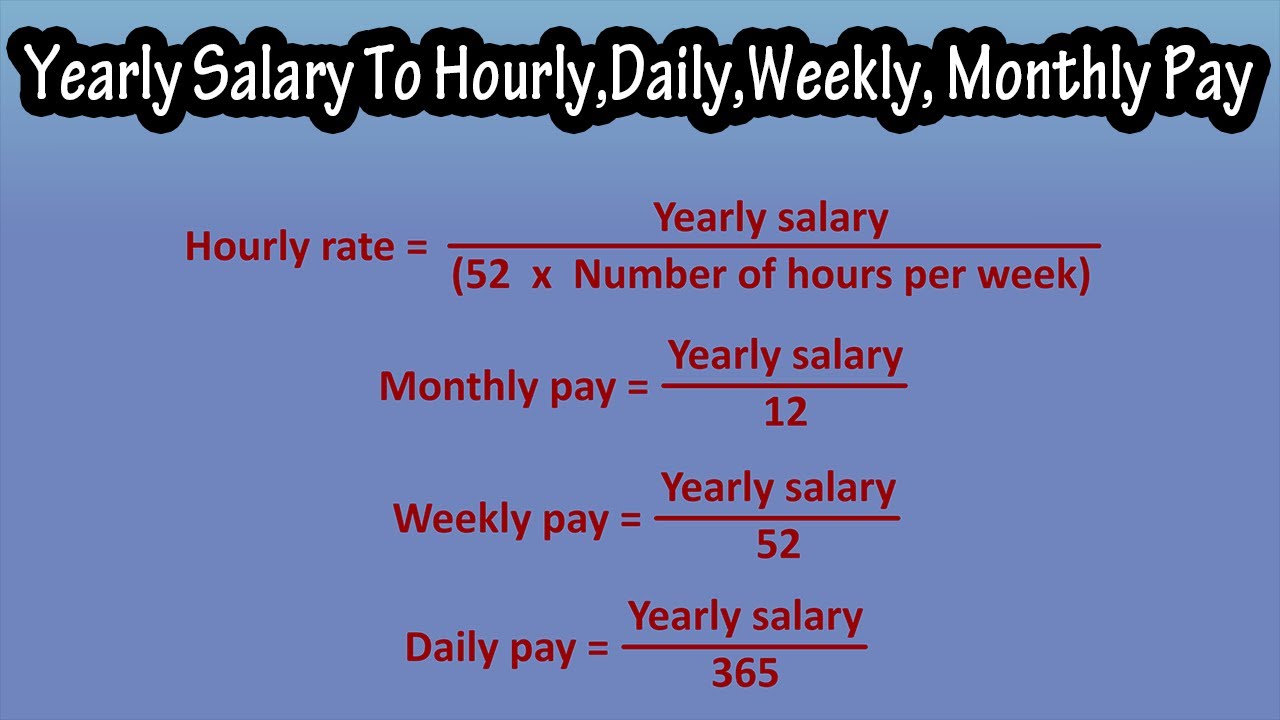

So, $6,000 a month? You just gotta multiply that bad boy by 12. Twelve months in a year, folks. Still with me? Don't worry, there won't be a pop quiz.

Must Read

Ready for the earth-shattering revelation? Drumroll please… It's… $72,000 a year!

Boom! There you have it. Reginald was visibly underwhelmed. He was probably expecting, like, a million dollars. Reginald has high hopes.

Hold on, though! Before you dismiss $72,000 as "nothing special," let's consider a few things.

$72,000: Is It Scrooge McDuck Money?

Well, no. Probably not. Unless Scrooge McDuck is living on a very, very strict budget these days and downsizing from his money bin to a slightly-less-large-but-still-impressive storage unit filled with gold-plated bottle caps.

But is it good money? Absolutely! Let's break it down a little further.

Imagine what you could do with that: Pay rent (a necessity, unless you’re planning to live in a refrigerator box, which I strongly advise against). Buy groceries (ramen noodles get old, trust me). Maybe even afford a vacation that doesn't involve camping in your backyard (unless, you know, you're into that sort of thing).

It also depends heavily on where you live. $72,000 in New York City? You might be sharing a closet-sized apartment with three roommates and a very judgmental cat. $72,000 in, say, rural Nebraska? You might be living like royalty… or at least, a very comfortable duke.

Taxes: The Uninvited Party Guest

Now, here’s the buzzkill moment: Taxes. Uncle Sam always wants his cut. It’s like that annoying relative who shows up to every party and eats all the good snacks. You're never rid of them.

So, $72,000 isn't exactly what you'll be taking home. Expect to see a chunk of that disappear for federal, state, and maybe even local taxes. It’s a necessary evil, but still…evil.

A good rule of thumb (and I'm pulling this rule of thumb straight out of thin air, so take it with a grain of salt the size of Rhode Island): expect to keep roughly 60-70% of that after taxes. So, maybe closer to $43,000 - $50,000 in your bank account annually.

The Real Question: What Can You Do With It?

The truly important thing isn’t just the number itself, but what you do with that money. Are you saving for retirement? Paying off debt? Investing in your future? Buying that inflatable T-Rex costume you've always dreamed of?

Because let's be honest, a good financial plan is better than all the money in the world (okay, maybe not ALL the money in the world, but you get my point). Reginald, for example, would probably spend it all on limited-edition Pokemon cards and those weird, squishy toys that are inexplicably popular. I, on the other hand, would invest wisely... after buying a slightly smaller inflatable T-Rex. For the children, of course.

So, back to my latte and Reginald's existential financial crisis. $6,000 a month is $72,000 a year. Is it life-changing wealth? Probably not. But it’s a solid foundation to build on. A stepping stone to, perhaps, one day affording a latte that doesn't make you question your life choices. Now, if you'll excuse me, I think I see a limited-edition Pokemon card I need to… invest in.