2 Hard Inquiries From Same Company

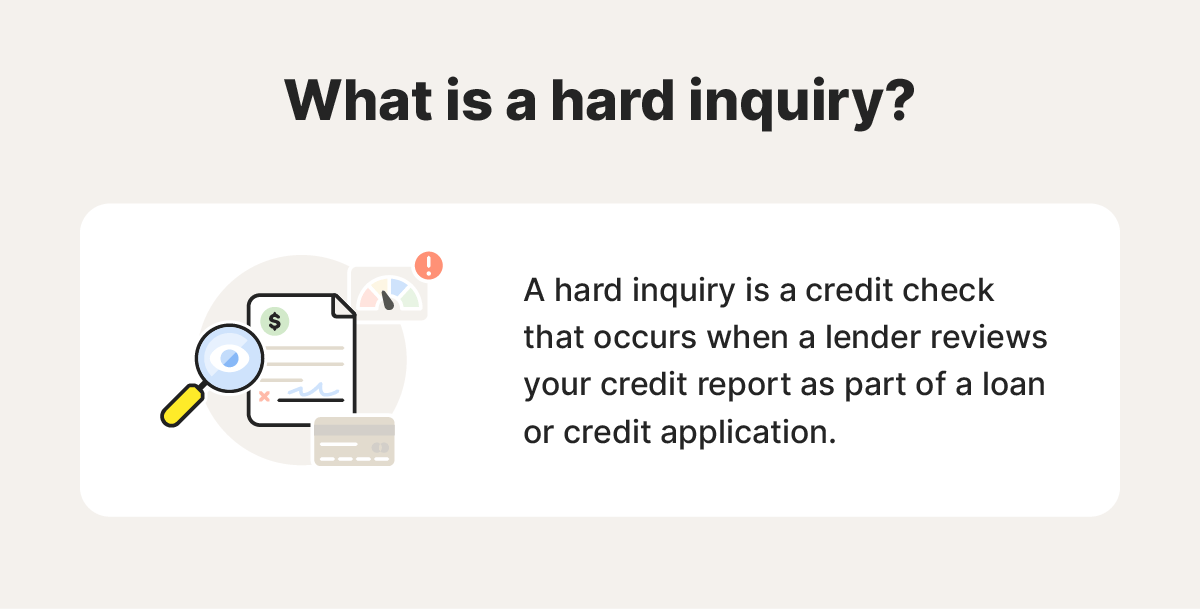

The appearance of multiple hard inquiries from the same company on a consumer's credit report, particularly within a short timeframe, can trigger confusion and concern. While seemingly innocuous, this scenario carries implications for credit scores, financial planning, and consumer trust. Understanding the underlying causes, the potential effects, and the broader implications is crucial for both consumers and businesses.

Causes of Multiple Hard Inquiries

Several factors can contribute to the occurrence of duplicate hard inquiries from a single company. These reasons often stem from legitimate business practices, technological glitches, or procedural errors. Analyzing these causes provides a clearer understanding of the phenomenon.

Application Processes and Pre-Approval Offers

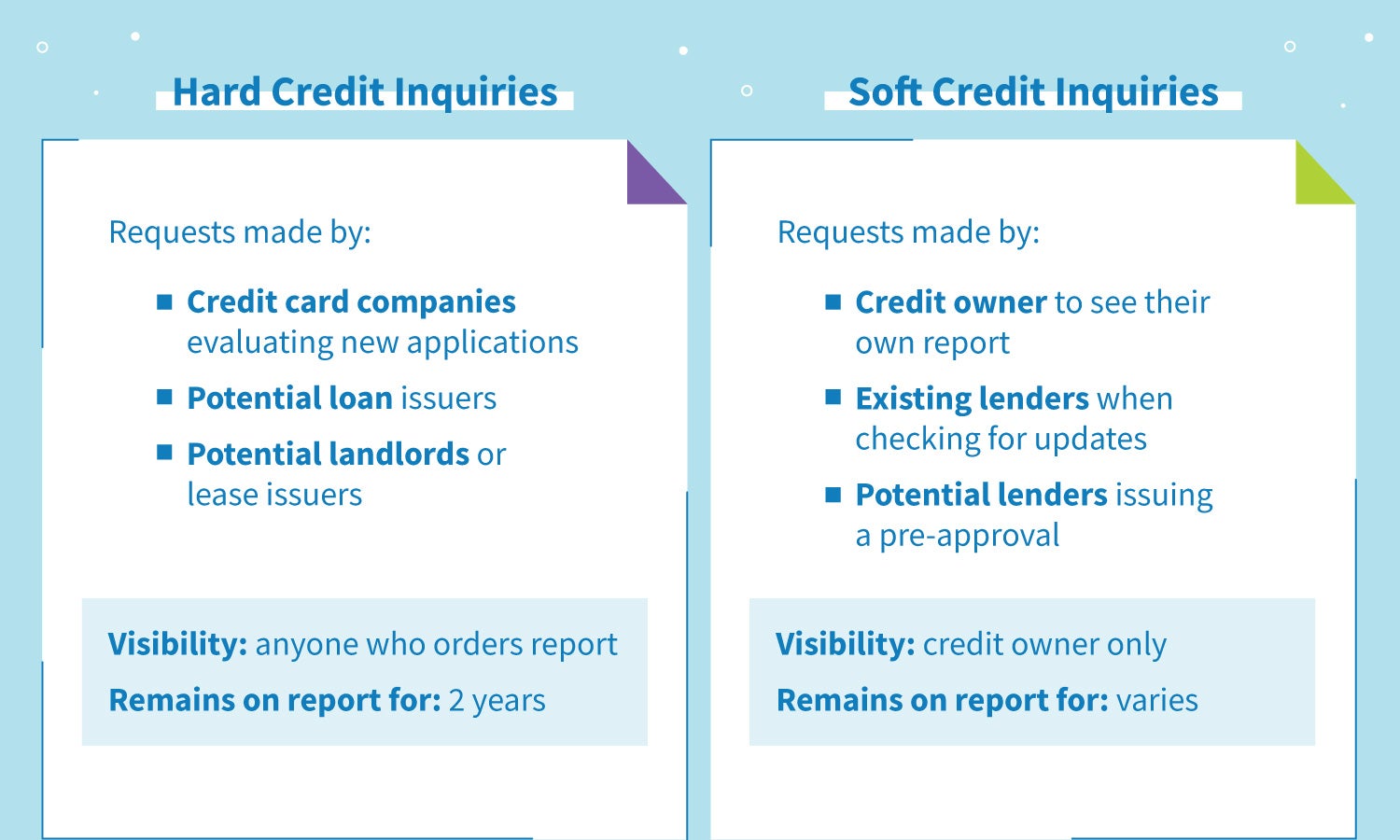

One of the most common reasons for multiple inquiries arises from the structure of the application process itself. For example, when applying for an auto loan or a mortgage, a lender might check credit at various stages. An initial inquiry could occur during the pre-approval process to estimate the potential loan amount and interest rate. A subsequent inquiry might be triggered when the consumer formally submits their application, solidifying their intent to secure the loan. This is often standard practice, but the multiple inquiries might not always be clearly communicated to the consumer.

Must Read

Similarly, pre-approved credit card offers can generate inquiries if the consumer responds and proceeds with the application. Some companies may perform a soft inquiry for the pre-approval itself, followed by a hard inquiry if the consumer decides to accept the offer and formally apply. The initial soft inquiry, not impacting the credit score, is often invisible to the consumer until they pull their credit report and observe the subsequent hard inquiry.

Third-Party Vendors and Affiliate Networks

Companies frequently employ third-party vendors or affiliate networks to market their products or services. In these arrangements, multiple entities might access consumer credit information. For example, an auto dealer may submit a loan application to several lenders through a network to find the best interest rate. Each lender accessing the credit report could register a hard inquiry. Although the consumer only applied once, the report might show multiple inquiries from different financial institutions, all related to the same underlying credit application. The lack of transparency in these networks can be a significant source of confusion and frustration for consumers.

System Errors and Data Duplication

Technological glitches and data entry errors can also lead to multiple hard inquiries. A system malfunction could cause a single application to be processed multiple times, generating duplicate inquiries. Similarly, human error during data entry could result in the same application being submitted more than once. While these errors are often unintentional, they can still negatively impact a consumer's credit report. Ensuring robust data management practices and regular system audits can mitigate this risk.

Fraudulent Activity

In rare instances, multiple hard inquiries from the same company may be a sign of fraudulent activity. If someone is attempting to open accounts or apply for credit in another person's name, they might submit multiple applications through various channels, resulting in numerous inquiries. While less frequent than other causes, this scenario underscores the importance of regularly monitoring credit reports and promptly reporting any suspicious activity to the credit bureaus.

Effects on Credit Scores and Financial Well-being

Multiple hard inquiries, even from the same company, can have tangible effects on a consumer's credit score and overall financial well-being. Understanding these effects is crucial for making informed decisions about credit applications and for actively managing one's credit profile.

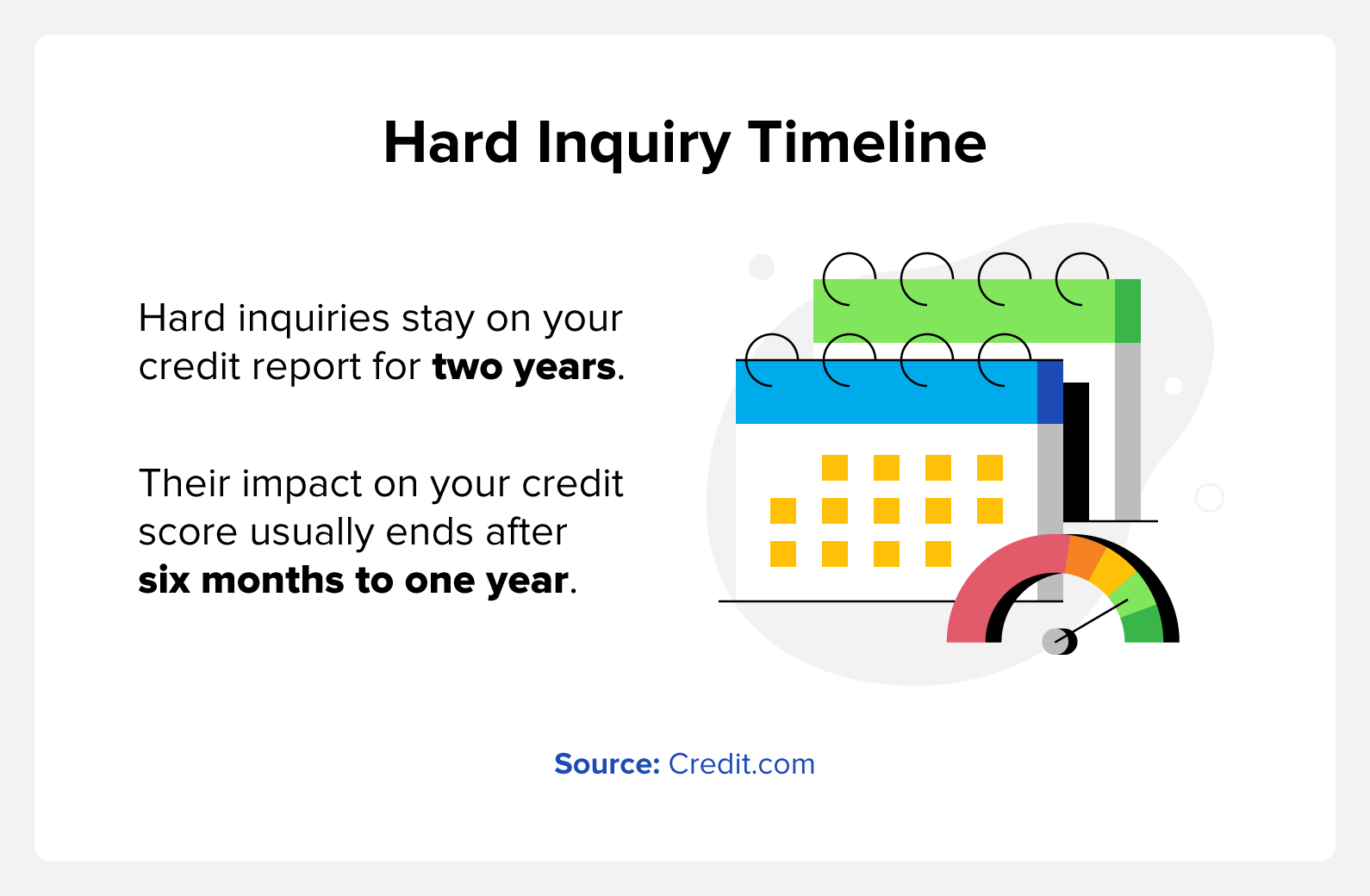

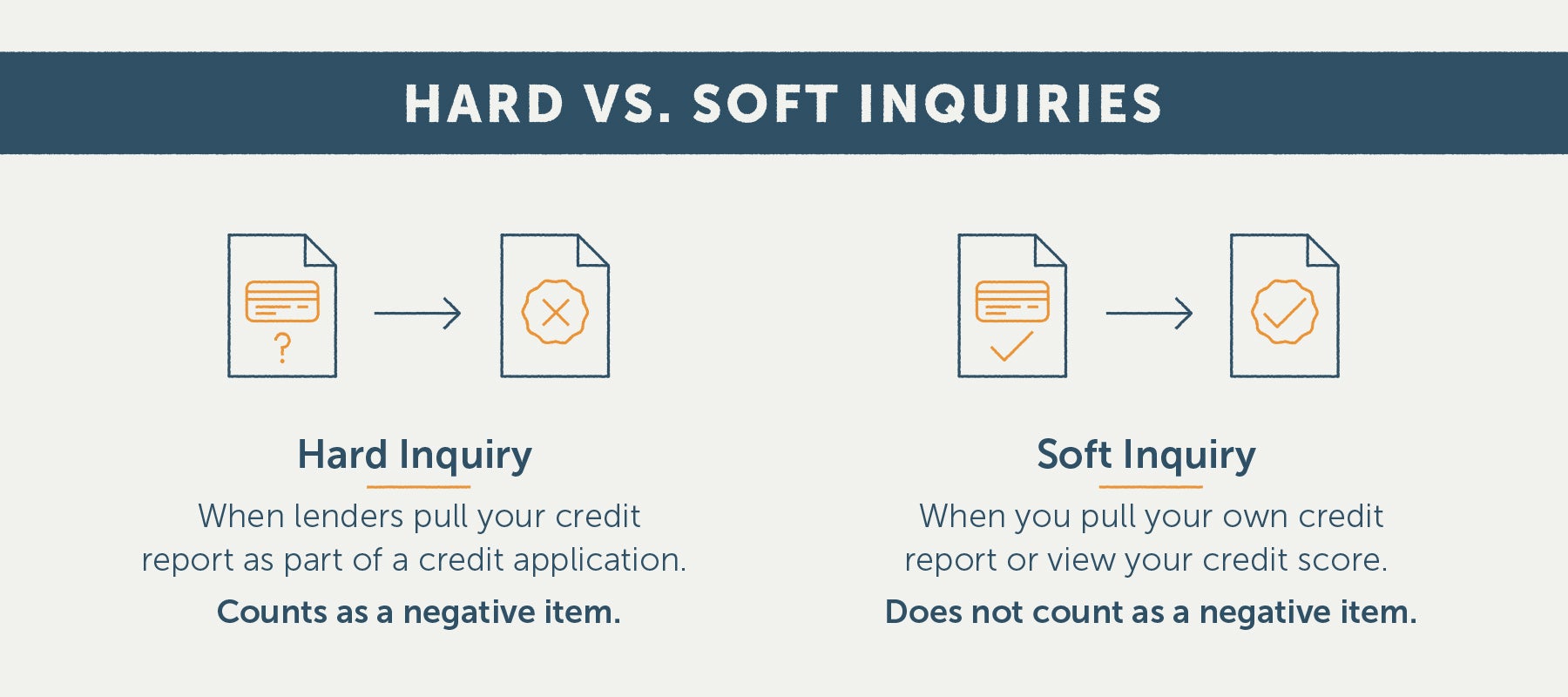

According to FICO, hard inquiries typically have a small, short-term impact on credit scores. While a single hard inquiry usually causes a negligible drop (often less than five points), multiple inquiries within a short period can cumulatively reduce the score more significantly. This is especially true if the inquiries are for different types of credit, as it can suggest a higher level of financial risk.

While FICO and VantageScore algorithms are designed to recognize rate-shopping behavior (e.g., multiple auto loan or mortgage inquiries within a 14-45 day window are often treated as a single inquiry), this protection does not automatically apply to all types of credit. Multiple credit card applications, even if submitted around the same time, may be viewed as separate attempts to increase available credit, potentially raising concerns about credit management.

Furthermore, the presence of multiple inquiries can deter other lenders from extending credit. A lender might interpret numerous recent inquiries as a sign that the consumer is actively seeking credit from multiple sources, potentially indicating financial instability or a higher risk of default. This can result in loan denials, higher interest rates, or less favorable terms. The cumulative effect can hinder a consumer's ability to access affordable credit and achieve their financial goals, such as purchasing a home or securing a low-interest loan for education.

Implications for Businesses and Consumer Trust

The practice of generating multiple hard inquiries, even if unintentional, carries significant implications for businesses and their relationship with consumers. The ethical and reputational consequences of this practice should not be underestimated.

Firstly, repeated hard inquiries can erode consumer trust. When a consumer observes multiple inquiries from the same company, it can create the impression of aggressive or deceptive lending practices. This can damage the company's reputation and lead to negative online reviews and word-of-mouth criticism. In an era where consumer trust is paramount, businesses must prioritize transparency and clarity in their credit inquiry practices.

Moreover, regulatory scrutiny is increasing in the realm of consumer credit. The Consumer Financial Protection Bureau (CFPB) actively monitors lending practices and enforces regulations designed to protect consumers from unfair or deceptive practices. Companies that engage in practices that lead to unwarranted multiple hard inquiries may face investigations, fines, or other regulatory actions.

Therefore, compliance with consumer protection laws is not just a legal obligation but also a business imperative.

Finally, businesses have a responsibility to educate their customers about the credit inquiry process. Providing clear and concise information about when and why credit checks are performed can help manage consumer expectations and prevent misunderstandings. This proactive approach can foster trust and strengthen the relationship between businesses and their customers. It involves clearly articulating the different stages of the application process, the role of third-party vendors, and the potential impact on credit scores.

Broader Significance

The issue of multiple hard inquiries from the same company highlights the broader challenges of transparency and accountability in the consumer credit ecosystem. It underscores the need for greater consumer awareness, more robust data management practices, and stricter regulatory oversight. The impact of credit scores extends far beyond obtaining loans or credit cards; they affect access to housing, employment, and even insurance. Therefore, ensuring the accuracy and fairness of credit reporting is crucial for promoting economic opportunity and financial well-being.

The prevalence of digital applications and online lending has only amplified the potential for multiple inquiries. As technology continues to evolve, businesses must adapt their practices to ensure that credit checks are performed ethically and responsibly. This includes implementing safeguards to prevent system errors, providing clear disclosures to consumers, and actively monitoring third-party vendors. The future of consumer credit depends on a commitment to transparency, fairness, and consumer protection. Only then can we build a credit ecosystem that benefits both businesses and consumers alike.